In 2003, Martin Lewis launched MoneySavingExpert.com from his living room with a reported initial outlay of £80–£100 (sources vary between the web design fee specifically and total startup costs)—an amount that would ultimately generate one of the highest-return digital intellectual property originations in UK media history. What began as a bootstrapped consumer advice platform, architected around hyper-focused search intent and zero external venture capital, escalated into a high-margin media powerhouse commanding an enterprise valuation of up to £87 million within nine years.

The forensic significance of this case lies not merely in the multiplication of capital, but in the structural integrity of the underlying asset: Lewis engineered a trust-based traffic engine that converted organic consumer grievance into monetizable engagement, all while preserving absolute editorial independence through a binding editorial code that prevented the typical post-acquisition erosion seen in private equity media buyouts.

The Sunday Times Rich List historically benchmarks Lewis’s baseline net worth at £123 million. While this figure serves as a static historical benchmark rather than an active live valuation, it reflects a foundational wealth architecture built on realized liquidity events, diversified asset holdings, and disciplined philanthropic carve-outs. Unlike standard internet entrepreneurs who scale via aggressive venture capital injections that dilute equity early, Martin Lewis represents the organic, bootstrapped operational model—converting hyper-focused search intent into a high-margin consumer media powerhouse. His trajectory offers a definitive blueprint for how a media asset can be scaled from zero capital to institutional liquidity without losing its core trust engine, making the Lewis Capital Escalation a mandatory study for any audit of UK digital media wealth creation.

The Wealth Timeline: The Lewis Capital Escalation

The £87M Exit Structure: Dissecting the Moneysupermarket.com Acquisition Model

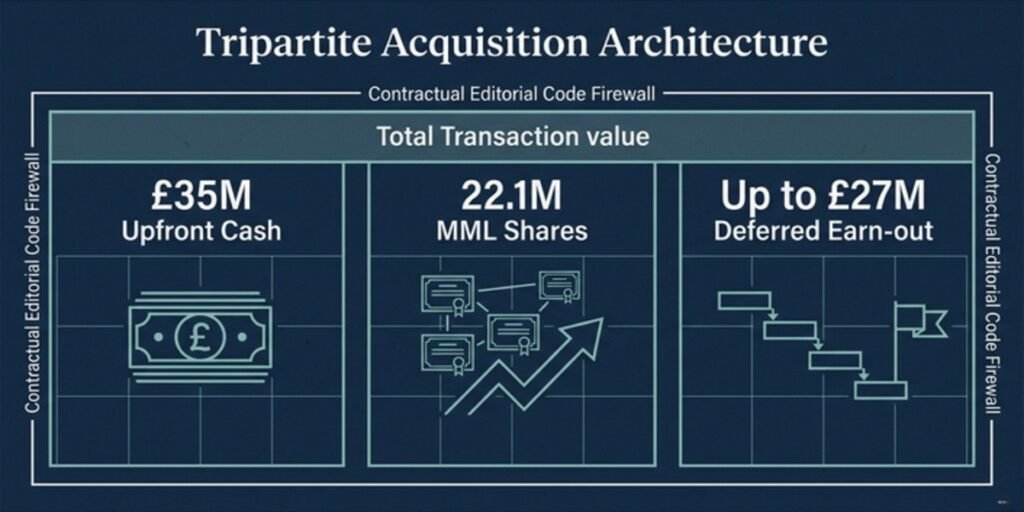

The acquisition of MoneySavingExpert.com by Moneysupermarket.com Group PLC (now MONY Group), announced in June 2012 and legally completed on 21 September 2012, represents a masterclass in structured deal architecture, blending immediate liquidity with long-term upside preservation. The transaction was not a simple cash purchase but a tripartite consideration mechanism designed to align Lewis’s continued operational input with the parent group’s performance metrics.

At closing, Lewis received £35 million in upfront cash, approximately 22.1 million MML shares valued at prevailing market rates, and deferred consideration of up to £27 million contingent on earn-out performance and operational milestones — of which £19.2 million was ultimately confirmed as payable to Lewis when the earn-out matured — as detailed in the official RNS acquisition announcement.

This equity-heavy structure served dual strategic functions. For Moneysupermarket.com, the issuance of 22.1 million shares acted as a retention mechanism, ensuring Lewis remained tethered to the asset’s editorial and commercial trajectory. For Lewis, the share component preserved upside mobility, allowing him to participate in the parent group’s market capitalization growth without surrendering all equity in his own creation. The deferred consideration—reportedly subject to traffic and revenue benchmarks—functioned as a classic earn-out security mechanism, protecting the acquirer from overpayment while incentivizing Lewis to maintain the editorial standards that had generated MSE’s 15-million-user ecosystem at the time of acquisition.

Critically, Lewis did not exit operationally. He retained the role of Editor-in-Chief under a binding editorial code that guaranteed MSE’s editorial independence from commercial interference. This was not a ceremonial title; it was a contractual firewall that prevented Moneysupermarket.com from redirecting MSE’s high-intent consumer traffic toward its own comparison products in ways that would degrade user trust. The preservation of this editorial moat is central to understanding why MSE’s traffic engine did not suffer the typical post-acquisition decay seen when media brands are absorbed into larger corporate entities. The site maintained its organic search dominance because the underlying content architecture remained user-centric rather than commercially co-opted.

You May Also Like to read–

- Pippa Middleton’s Net Worth & Hedge Fund Multipliers

- How to Find Real Celebrity Net Worth via Companies House Filings: Forensic Wealth Tracking

- Mega-Deals and Venture Pivots: Auditing Nick Candy’s Net Woth, Real Estate and Capital Portfolio in 2026

The 2015 Share Liquidation and Present Financial Asset Portfolio

In July 2015, Lewis executed a strategic secondary market placement, liquidating 9 million MML shares—representing just over half of his remaining post-acquisition shareholding—for £25.2 million in cash. The block sale, conducted through institutional placement, represented a decisive diversification maneuver, converting concentrated public equity exposure into liquid capital capable of deployment across conservative UK wealth management systems, high-end real estate holdings, and treasury balances.

The timing of the 2015 liquidation merits forensic attention. Lewis had already received his £35 million upfront cash payment in 2012, and by mid-2015 the deferred consideration mechanisms had largely matured. The July share sale therefore represented a deliberate portfolio rebalancing—locking in gains from MML’s market performance while reducing single-stock concentration risk. Notably, Lewis did not liquidate his entire position; he retained a significant minority stake, allowing continued participation in dividend flows and share price appreciation while insulating his personal balance sheet from sector-specific volatility in the UK price-comparison market.

Post-2015, Lewis’s consolidated wealth trajectory stabilized into a diversified holdings structure. According to the Sunday Times Rich List, his net worth stands at £123 million—a figure reflecting not active entrepreneurial risk but the compounding of realized liquidity events, conservative investment returns, and strategic asset allocation. His present portfolio is understood to include substantial London residential property, managed fund exposures through UK private wealth institutions, and liquid treasury reserves. The operational income from his ITV broadcasting contracts, syndicated journalism, and publishing royalties provides additional cash-flow layering, though these represent marginal contributions relative to the capital base established through the MSE exit.

The Philanthropic Carve-Out: Institutionalizing Wealth Distribution

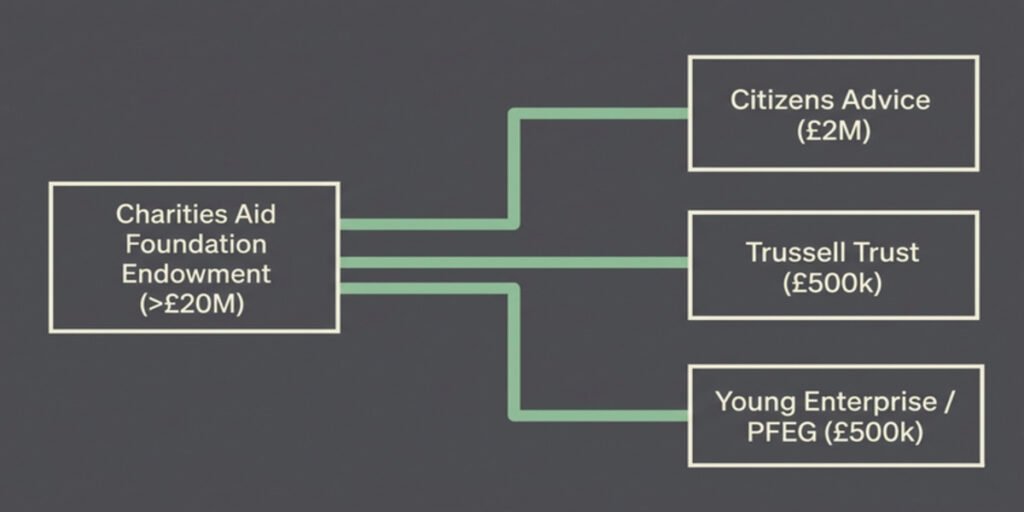

Parallel to his wealth accumulation, Lewis executed one of the most systematically documented philanthropic carve-outs in UK media history. In June 2012, concurrent with the MSE sale announcement, he pledged £10 million to charitable causes—a commitment that has since escalated through gift-aid amplification and share appreciation to exceed £20 million in total charitable capital. The fund is administered through the Charities Aid Foundation, a structure Lewis deliberately chose to publicize as a model for high-net-worth giving, retaining control over disbursement while ensuring all distributions flow exclusively to registered charities.

The forensic flow of capital reveals a strategic targeting of underfunded institutional infrastructure. Citizens Advice received £2 million across two major tranches: an initial £1 million in 2012, split proportionally across England and Wales (£615,000 cash plus 215,703 MML shares), Scotland (£85,000 cash), and Northern Ireland (£50,000 cash); and a subsequent £1 million pledge in 2015 following the share liquidation. This targeting was deliberate—Lewis explicitly directed capital toward Citizens Advice at a moment when government austerity measures had severed debt-counselling funding, using his private wealth to expose public-sector funding gaps.

The Trussell Trust and the Personal Finance Education Group (now a Young Enterprise sub-brand) each received £500,000 endowments. The Trussell Trust allocation funded the rollout of financial triage services across UK food banks, building on a successful £100,000 pilot that demonstrated measurable outcomes in debt reduction and service uptake. The PFEG endowment specifically underwrote three years of the My Money Week project, sustaining financial education in schools at a critical juncture when many donors incorrectly assumed curriculum inclusion had eliminated the need for supplemental charitable support. Additional disbursements included £100,000 to Mind for mental health work and smaller allocations to the Royal National Institute of Blind People and Winston’s Wish.

Also read:

- Sarra Kemp: Everything About Chris Hoy’s Wife and Her Remarkable Story

- Matteo Mantegazza: The Son of Award-Winning Actress Greta Scacchi

- Alice Bamford: Film Producer, Global Environmental Educator, and Scion of Britain’s Billionaire Bamford Dynasty

The “Trust Premium” Valuation: Editorial Independence as Enterprise Value

The conventional private equity acquisition model for digital media assets follows a predictable decay curve: post-sale traffic erosion of 15–30 percent within eighteen months as editorial integrity is compromised by commercial redirect strategies, native advertising infiltration, and affiliate link dilution. The MSE case defies this pattern. By negotiating a binding editorial code that guaranteed absolute independence from Moneysupermarket.com’s commercial operations, Lewis preserved the underlying trust architecture that had generated MSE’s search-engine dominance and 16-million-monthly-user ecosystem at its peak.

This “trust premium” functioned as a hidden valuation multiplier. While not explicitly priced into the 2012 transaction, it protected the acquirer’s return on investment by preventing the typical post-acquisition traffic collapse. MSE’s editorial code—ensuring no commercial interference in content decisions, no preferential placement of Moneysupermarket.com products, and no dilution of consumer-revenge journalism—maintained the site’s high-intent user base. The traffic engine, built on template-letter downloads, PPI reclaim guides, and energy-switching tools, continued to generate organic engagement because users recognized that the editorial product had not been captured by its corporate parent. For wealth auditors, this represents a critical lesson: in consumer media, editorial independence is not merely an ethical stance but a balance-sheet asset that preserves enterprise value post-liquidity.

The Supercomplainant Status Asset: Systemic Influence as Competitive Moat

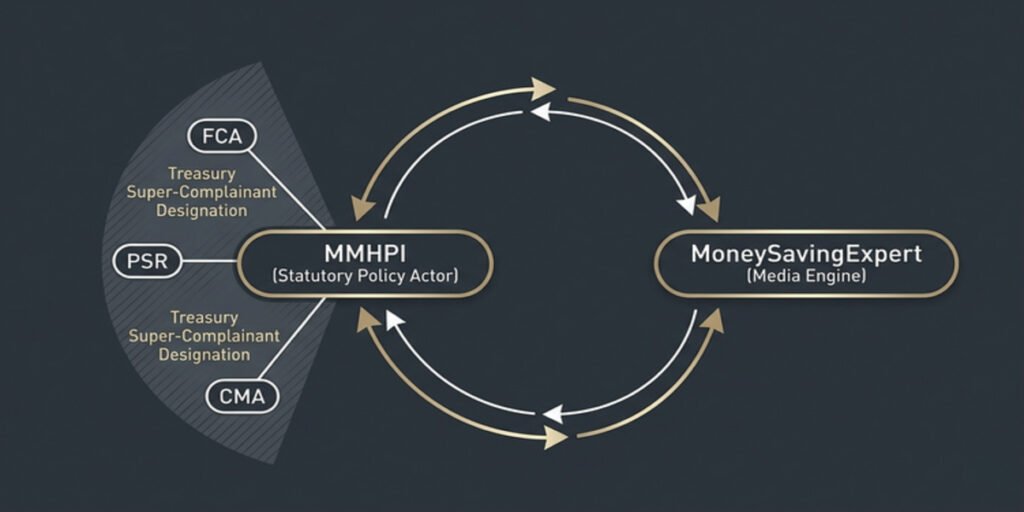

In March 2026, The Financial Services (Designated Consumer Body and Designated Representative Body) Order 2026 designated by HM Treasury formally took legal effect, awarding the Money and Mental Health Policy Institute (MMHPI) expanded super-complainant status. This milestone granted the charity fast-track powers to lodge complaints directly with the Financial Conduct Authority (FCA) and the Payment Systems Regulator (PSR).

The enterprise value of this status cannot be overstated. Super-complainant designation transforms MMHPI from a standard advocacy charity into a systemic policy actor with statutory leverage over UK financial regulation. The Treasury’s designation instrument explicitly recognizes the institute’s capacity to identify market-wide consumer harms—particularly at the intersection of mental health vulnerability and predatory financial practices—and compel regulatory investigation without the procedural friction faced by standard complainants. Crucially, as outlined by MoneySavingExpert’s Official Announcement, this expansion builds upon MMHPI’s initial super-complainant status granted by the Competition and Markets Authority (CMA) in 2025. As a result, the charity now operates uniquely across the entirety of the UK’s tripartite regulatory architecture: competition, financial conduct, and payment systems.

For the Lewis corporate ecosystem, this status functions as a competitive moat that reinforces the core MSE brand’s systemic influence. The institute’s research outputs—on topics ranging from bipolar spending-spree prevention to debt-collection trauma—feed directly into MSE’s editorial pipeline, generating proprietary content that cannot be replicated by rival consumer sites. The policy work legitimates the journalism; the journalism funds the policy work through audience scale and donation flows. This symbiotic structure creates a self-reinforcing influence loop that extends Lewis’s consumer champion positioning from media into statutory governance, an asset class that traditional net-worth calculations cannot fully capture but that fundamentally underpins the £123 million valuation’s sustainability.

Frequently Asked Questions

Q: How much did Martin Lewis sell MoneySavingExpert for?

Q: What is Martin Lewis’s net worth according to the Sunday Times Rich List?

Q: Does Martin Lewis still own MSE?

Q: Why is the Money and Mental Health Policy Institute’s super-complainant status considered an enterprise “moat”?

Q: How exactly was the initial capital outlay structured in 2003?

Disclaimer & Editorial Notes

This profile functions strictly as an independent forensic corporate case study and public asset audit. All financial data, transaction milestones, and net worth indexing are compiled exclusively from high-authority public records, statutory regulatory filings, and historical media indexes. Elites Mindset operates with absolute editorial independence and maintains no corporate affiliation, endorsement, or commercial relationship with Martin Lewis, MoneySavingExpert.com, or MONY Group PLC. The insights provided herein are for educational and analytical purposes only and do not constitute financial, legal, or investment advice.

You May Be Interested Exploring These Profiles–

- Who is Louise Bonsall? Michael Owen’s Wife & the Force Behind the Owen Dynasty

- Cassie randolph net worth

- Ifet Anwar: Leading Scottish Property Solicitor and Advocate

- Bill Gaither net worth