For serious analysts, family offices, and investigative journalists, the UK Companies House registry provides something no celebrity wealth calculator can: legally binding, audited financial statements prepared under UK GAAP, signed off by directors, and subject to penalties for false disclosure. This guide provides the definitive forensic blueprint for extracting verified corporate wealth data directly from the source — bypassing the media speculation that conflates brand valuations, unverified real estate rumours, and inflated estimates.

The internet is awash with platforms that claim to pinpoint the fortune of public figures down to the last pound. These aggregators pull from speculative media reports and unverified sources. The result is often a fiction masquerading as financial journalism: a performer publicly estimated at £200 million may, in reality, hold a fraction of that in liquid and non-liquid corporate assets, while the remaining phantom wealth exists only in the imagination of content farms. Unlike third-party wealth trackers, Companies House filings are statutory documents. This guide shows you how to use them.

Note: The characteristics above reflect common practices observed across leading third-party celebrity net worth platforms that do not utilise statutory filings.

Critical Distinction: A Companies House balance sheet reveals the net corporate assets of a specific corporate entity, not total personal net worth. Private real estate, offshore holdings, and personal chattels exist outside this framework.

The Personal Service Company (PSC) Blueprint: How UK Celebrities Structure Their Wealth

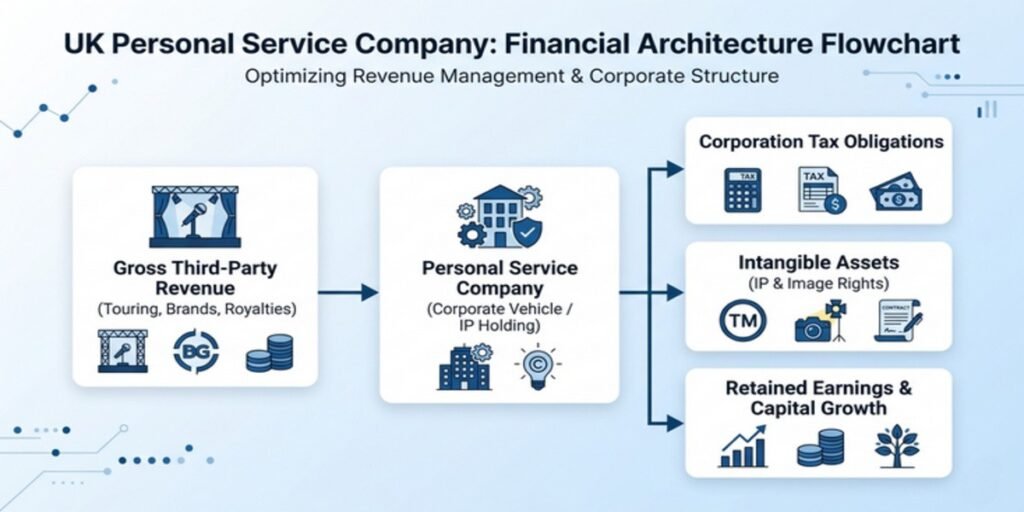

High-net-worth public figures do not typically receive performance fees, royalties, or endorsement income as personal salary. Instead, they incorporate private limited companies—commonly known as personal service companies or loan-out companies—that contract with studios, record labels, and brands directly. The celebrity becomes an employee or director of their own company, which then “loans out” their services to third parties. This structure is the foundational architecture of entertainment industry wealth management in the UK.

The mechanics are deliberate and financially sophisticated. When Ed Sheeran records an album or licenses his catalogue, the label does not pay Ed Sheeran the individual. It pays Gingerbread Man Records Limited, a confirmed UK-registered corporate vehicle (company number 09518102) through which his music revenue is channelled. Similarly, Dua Lipa’s publishing interests are managed through Radical22 Publishing Limited (Company number 15102343), a company incorporated in 2023 and fully owned by the artist. These entities convert what would be personal income taxed at marginal rates into corporate revenue subject to corporation tax, with the retained earnings held within the company for reinvestment, distribution, or long-term capital growth.

Beyond tax optimisation, these structures serve critical asset protection and intellectual property functions. A musician’s back catalogue, a comedian’s special rights, or an actor’s image licensing agreements can be held as intangible assets on the company’s balance sheet. The company can then license these rights globally, with revenue flowing into a UK-regulated corporate vehicle that maintains a clear audit trail. For family offices and wealth preservation strategists, this structure also facilitates multi-generational planning: shares in the personal service company can be transferred to trusts or family members, allowing wealth to cascade without triggering immediate personal inheritance tax events on the underlying IP value.

While generic media outlets rely on flawed, unverified third-party estimates for icons like Ed Sheeran or Dua Lipa, sophisticated analysts look directly at entities like Gingerbread Man Records Limited or Radical22 Publishing Limited on Companies House to evaluate audited, legally binding financial statements. These filings expose cash reserves, debt obligations, and shareholder funds with a precision that no celebrity gossip portal can replicate.

LLPs vs. Limited Companies: It is worth noting that many entertainment industry vehicles are structured as Limited Liability Partnerships (LLPs) rather than private limited companies. LLP accounts are publicly available on Companies House but follow different filing requirements and disclosure rules. While this guide focuses on limited companies for clarity, researchers should recognise that high-profile tour managers and production entities often use LLP structures, and the same principles of public record access apply.

Step-by-Step Guide: Searching the Companies House Registry for High-Profile Directors

The Companies House search portal is a free, public government database. It requires no registration for basic searches and provides immediate access to officer histories, filing deadlines, and statutory accounts. The following operational protocol ensures you identify the correct individual and their complete corporate footprint.

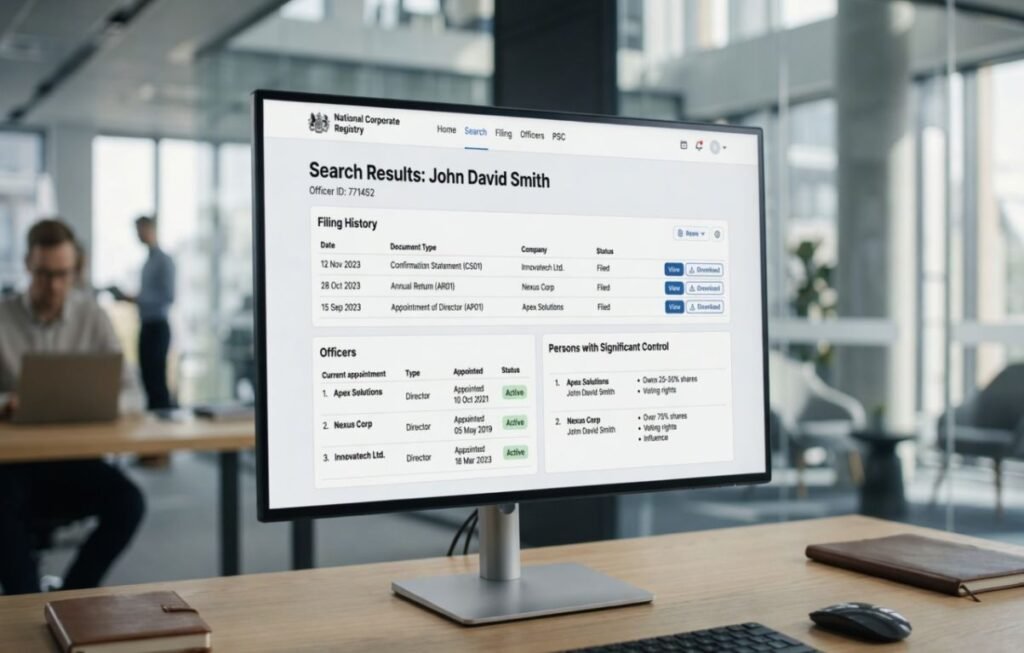

Step 1: Search by Legal Name Under the “Officers” Tab

The most common research error is searching for a celebrity’s stage name or a known trading name. Companies House indexes individuals by their legal name as it appears on official identification. Navigate to the main search bar and enter the individual’s full legal name—Edward Christopher Sheeran, not “Ed Sheeran”; Dua Lipa, fortunately, uses her birth name professionally. Select the “Officers” tab to filter results to individuals rather than companies. The system will return a list of matching names, each showing a partial date of birth (month and year only), nationality, and country of residence. Use these data points to confirm identity, cross-referencing with known biographical information. For example, Dua Lipa’s director profile lists her date of birth as August 1995, her role as active director of Radical22 Publishing Limited, and Dua Lipa was appointed as a director of Radical22 Publishing Limited on 3 March 2023.

Step 2: Map All Current and Historical Appointments

Clicking the individual’s name reveals their complete appointment history—every company they currently direct, every company they have resigned from, and the precise dates of those appointments. This timeline is invaluable. A celebrity who resigned from a touring company in 2022 but remains director of a holding company in 2025 may have shifted revenue streams or restructured for tax efficiency. Pay attention to “active” versus “dissolved” company statuses. A dissolved company may have distributed its assets before closure, or it may have been struck off for non-filing—a critical red flag in any forensic analysis.

Step 3: Identify the Company Number and Access Filing History

Each company is assigned a unique registration number. Once you identify the relevant corporate vehicle, click through to the company overview page. The “Filing history” tab contains every document ever submitted to Companies House: annual accounts, confirmation statements, changes of registered office, and officer appointments. For wealth extraction, the annual accounts are your primary target. These are uploaded as PDF documents and can be downloaded immediately.

In addition to annual accounts, each company files an annual confirmation statement (formerly the annual return). This document confirms the registered office, standard industrial classification (SIC) codes, and share structure. Because it must be filed within 14 days of the confirmation anniversary, it is often more current than the statutory accounts — making it the preferred first check for verifying current PSC and shareholding status. Researchers should cross-reference the confirmation statement to verify that the PSC register and shareholdings remain unchanged since the last accounts filing.

The PSC Register Loophole: Verifying Beneficial Ownership

Every company profile contains a “People” tab with two subsections: “Officers” and “Persons with significant control.” The PSC register is where forensic researchers verify who actually owns the capital. A Person with Significant Control is defined as an individual who holds more than 25% of shares or voting rights, holds the right to appoint or remove a majority of the board, or otherwise exercises significant influence or control.

If a celebrity owns 75% or more of the shares, they exercise outright control of the capital surplus and can unilaterally direct dividend policy or asset liquidation. If shares are split with family members, managers, or trusts, the wealth allocation must be mathematically adjusted. For instance, if a celebrity holds 50% and their sibling holds 50%, the celebrity’s accessible corporate wealth is precisely half the net assets figure—not the headline total. The PSC register discloses exact ownership percentages, the nature of control, and the date the individual became a PSC. This transforms a raw balance sheet figure into a personally attributable wealth calculation.

The Multiple-Entity Trap: Aggregating the True Corporate Footprint

Mega-celebrities rarely operate through a single company. An elite musician may maintain separate entities for touring, merchandise, music publishing, recording royalties, and personal branding. Each entity files its own statutory accounts. To calculate the true total corporate footprint, you must aggregate the Net Assets (Shareholders’ Funds) across every active entity where the individual holds significant control.

This requires systematic cross-referencing. From the individual’s officer profile, identify every active directorship. Download the latest annual accounts for each. Extract the Net Assets figure from each balance sheet. Sum these figures, then apply ownership percentage discounts based on the PSC register data for each entity. The resulting aggregate represents the total legally verified corporate wealth attributable to the individual across their entire UK corporate structure. Failing to conduct this aggregation is perhaps the most common error in amateur celebrity wealth analysis—it produces a figure that may understate true corporate wealth by 60% or more.

Decoding the Balance Sheet: Calculating Net Assets and Retained Earnings

Once you have downloaded the PDF filing, you are looking at a statutory balance sheet prepared under either FRS 105 (micro-entities), Section 1A of FRS 102 (small companies), or full FRS 102 (larger entities). Regardless of the standard, the fundamental wealth equation remains constant:

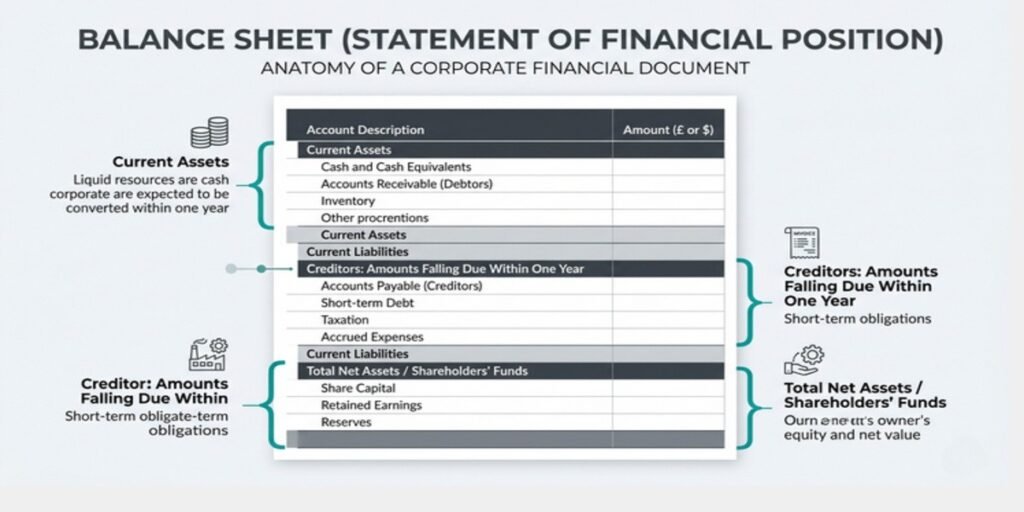

Net Assets = Total Assets − Total Liabilities

This figure appears on the balance sheet as “Total Net Assets” or, more commonly, as “Capital and Reserves” or “Shareholders’ Funds.” It represents the baseline, legally verified book value of the company’s accumulated wealth—the money that would theoretically remain if all assets were liquidated and all liabilities settled today.

To understand the composition of this wealth, you must dissect the line items above it. Under “Current Assets,” you will find “Cash at Bank and in Hand”—the true liquid cash reserves currently held by the corporate entity. This is not an estimate; it is the actual bank balance as of the financial year-end date. You will also find “Debtors”—money owed to the company by third parties, which may include unpaid invoice revenue from record labels, streaming platforms, or event promoters.

On the liabilities side, “Creditors: amounts falling due within one year” reveals immediate short-term debts, taxes owed, or deferred income obligations. A company may show £8 million in cash but £3 million in creditors, meaning the liquid position is weaker than the headline cash figure suggests. For entertainment companies, deferred income is particularly significant: if a tour was paid in advance but not yet performed, that cash sits on the balance sheet as an asset but is matched by a corresponding liability until the performance obligation is fulfilled.

“Retained Earnings” or “Profit and Loss Account” within the Capital and Reserves section represents the cumulative profits that have been reinvested in the company rather than distributed as dividends. This is the true store of historically generated wealth within the corporate vehicle. A company with £50 million in Shareholders’ Funds but only £2 million in retained earnings may have recently received a large capital injection or loan, whereas a company with £40 million in retained earnings has built that wealth organically over multiple financial years through trading profits.

The 9-Month Filing Delay Buffer: Understanding the Temporal Lag

A critical institutional constraint that separates amateur researchers from forensic analysts is the statutory filing timeline. UK private limited companies have up to nine months after their financial year-end to file accounts with Companies House. This means that the “current” accounts you are analysing today could reflect a financial position that is, in reality, up to twenty-one months old: a twelve-month trading period plus a nine-month filing extension.

For example, if a celebrity’s company has a financial year ending 31 March 2025, the accounts covering that period need not be filed until 31 December 2025. If you are conducting research in May 2026, the most recent filing available may still only reflect the position as of March 2025—fourteen months in the past. Major wealth events—tour completions, catalogue sales, or asset acquisitions—occurring after the balance sheet date will not appear until the subsequent filing cycle. Professional researchers must timestamp every data point and explicitly note the “as of” date of the underlying financial statements. Companies House data is a lagging indicator, not a live dashboard.

Micro-Entity Accounts vs. Full Filings: Navigating Disclosure Thresholds

Not all Companies House filings are created equal. The level of financial detail disclosed depends entirely on the company’s size classification under the Companies Act 2006, and the thresholds were significantly updated in April 2025. Under updated thresholds introduced by the Companies Act 2006 (Amendment) Regulations 2024 and effective from 6 April 2025, a company qualifies as a micro-entity if it meets at least two of the following three conditions: annual turnover not exceeding £1 million (up from £632,000), balance sheet total not exceeding £500,000 (up from £316,000), and average employees not exceeding 10.

Micro-entity accounts represent the most minimal disclosure regime permitted under UK law. These companies can file under FRS 105, which requires only a simplified balance sheet with minimal notes. Crucially, micro-entities are not required to file a profit and loss account with Companies House, meaning you cannot see turnover, cost of sales, or operating profit. The balance sheet will show aggregate fixed assets, aggregate current assets, aggregate creditors, and net assets—but no line-item breakdown of cash reserves, debtors, or liability composition. For a researcher attempting to assess an emerging creator’s corporate wealth, this opacity is a significant constraint.

Small companies, by contrast, file under Section 1A of FRS 102 and must provide more granular detail. A small company must meet at least two of: turnover not exceeding £15 million, balance sheet total not exceeding £7.5 million, and employees not exceeding 50. These entities file full balance sheets with detailed current asset and liability line items, allowing precise cash extraction and debt analysis. Major A-list talent—those with multi-million-pound touring revenues and extensive IP portfolios—almost invariably exceed micro-entity thresholds and therefore file comprehensive accounts that expose genuine financial depth.

When analysing a celebrity’s corporate structure, always check the filing type listed at the top of the accounts. If the document is labelled “Micro-entity accounts,” recognise that you are looking at a deliberately abbreviated picture. The true cash position may be buried within a single “Current Assets” lump sum, and the absence of a profit and loss account means you cannot verify revenue trajectory or profitability trends.

Final Accounts from Dissolved Companies

When a company is dissolved, its final accounts filed prior to dissolution remain permanently accessible on Companies House. These filings are forensically valuable: a celebrity who wound up a touring company after a major project may have filed accounts showing peak revenue, cash distribution, or asset transfers that inform the timeline of their wealth. Researchers should not ignore dissolved entities in the appointment history. Download the final available accounts and check the final balance sheet to see how remaining assets were disposed of before strike-off. Dormancy or dissolution does not erase the financial trail—it simply freezes it at the last statutory filing.

Frequently Asked Questions

Q1. Can you see a celebrity’s personal bank account on Companies House?

No. Companies House records only the corporate financial position of the registered limited company. The “Cash at Bank” figure refers strictly to the company’s business bank accounts, not the director’s personal current account, savings, or investment portfolios held in their individual name. Personal real estate, private vehicles, offshore trust assets, and individual stock market investments exist entirely outside the Companies House framework. The registry reveals corporate net assets, not total personal net worth.

Q2. What does it mean if a celebrity company is “Dormant”?

A dormant company is one that has had no significant accounting transactions during the financial year. For Companies House purposes, this means no active trading activity, no revenue generation, and no operational expenditure beyond permissible statutory administrative fees (such as filing fees or share capital adjustments at incorporation). A dormant company must still file annual dormant accounts and a confirmation statement, but these filings are minimal—typically a balance sheet showing only share capital with an accompanying note confirming dormancy.

If a previously active celebrity company suddenly pivots to filing dormant accounts, it may indicate that revenue streams have been systematically diverted to a new corporate vehicle, that a specific tour or project has concluded with no immediate successor, or that the individual is actively restructuring their affairs ahead of a major transaction. Dormancy does not indicate insolvency; it represents deliberate inactivity.

Q3. How accurate are Companies House filings for calculating total net worth?

Companies House filings are legally accurate for the specific corporate entities they govern, but they do not produce an all-encompassing personal net worth figure. The systemic accuracy of the corporate data itself is high: these are statutory documents, and false disclosure carries immediate civil and criminal penalties.

However, a forensic researcher must apply three critical adjustments to successfully extrapolate corporate net assets into personal wealth attribution:

- PSC Ownership Multiplier: Apply the exact Person with Significant Control (PSC) ownership percentage to account for split or fractional family shareholdings.

- Cross-Entity Aggregation: Systematically aggregate assets across all separate active entities (touring, merchandising, IP holding) using multiple-entity mapping protocols.

- Temporal Buffer Calibration: Adjust for the lagging indicator nature of the data introduced by the statutory nine-month filing buffer window.

Even following these analytical adjustments, the final balance sheet calculations explicitly exclude personal properties, individual investment portfolios, private pension pots, and any offshore wealth structures. Companies House provides the most accurate legally verifiable corporate wealth data available to the public—but it functions as a single component of net worth, not the entirety of it.

Related Forensic Wealth Audits

- • Broadcasting Capital: Sky Sports Pundit Salaries & Net Worth Audit

- • The Klutch Effect: Analyzing Rich Paul’s $1.4B Agency Value & Net Worth

- • Legacy Assets: A Comparative Study of British Sports Icons’ Net Worth