The 2026 regulatory environment has fundamentally altered the cost of inaccuracy. For Ultra High Net Worth (UHNW) entities, family offices, and private investment vehicles, the transition to SEC Inline XBRL (iXBRL) mandates is not merely a formatting exercise—it is a forensic restructuring of how financial truth moves from private ledger to public record. At the center of this transformation lies the “Original Quote Gap”: the precise moment when source data from treasury systems is manually extracted, copied, and pasted into disclosure documents, severing the digital audit trail.

In 2026, this gap represents a material weakness. When an auditor cannot trace a reported figure back to its originating system without encountering a human intermediary and a static spreadsheet, the filing entity faces heightened scrutiny, potential restatement risk, and the erosion of audit defensibility. The SEC’s 2026 validation protocols now enforce semantic consistency across filings, meaning a value tagged in one context cannot diverge in another without triggering EDGAR suspension protocols.

AI-ASSISTED EXECUTIVE SUMMARY (CLICK TO HIDE/SHOW)

Institutional Core: The transition to SEC Inline XBRL (iXBRL) in 2026 mandates a forensic shift for UHNW entities, moving from manual financial assembly to Zero-Touch Filing to ensure total data integrity.

The “Original Quote Gap” Risk: Manual data migration between treasury systems and disclosure documents is now classified as a material weakness. Failure to maintain an automated audit trail triggers heightened EDGAR validation scrutiny and restatement risk.

Forensic Stack Architecture:

- Immutable Lineage: By integrating Finastra (Source of Truth) with Workiva (Synchronization Layer), entities create a “Digital Birth Certificate” for every reported figure, enabling instant audit traceability.

- Semantic Consistency: 2026 protocols enforce identical tagging across all disclosure instances; automated linking ensures that a single ledger update cascades across 10-Ks, 10-Qs, and private reports simultaneously.

The Defensibility Premium: Real-time audit trails transform compliance from a retrospective burden into a defensive asset, shielding family offices from the volatility of “fishing expedition” audits and aggressive SEC enforcement.

Operational Efficiency: Eliminating the “Analyst-in-the-Middle” reduces revision fatigue and reporting latency, allowing complex multi-entity structures to meet accelerated filing deadlines with near-zero error rates.

The Strategic Pivot: In the 2026 landscape, transparency is the new SEO. UHNW entities that adopt automated, API-led disclosure frameworks secure a Trust Graph advantage that legacy manual models cannot replicate.

The architecture to close this gap has matured. Forward-looking UHNW entities are abandoning the “Analyst-in-the-Middle” model—where a human operator serves as a high-risk bridge between treasury data and regulatory output—in favor of Zero-Touch Filing infrastructure. This approach treats the disclosure document not as a destination for manually assembled data, but as a live, synchronized endpoint fed directly by the general ledger. The result is immutable data lineage: every number in a 10-K, 10-Q, or private stakeholder report carries a digital birth certificate that traces directly to the source system, timestamped, version-controlled, and free from manual transcription errors.

Intelligence Brief: The 2026 Disclosure Stack

Regulatory Horizon: All domestic filers must submit cover page, financial statement, footnote, and auditor information in Inline XBRL format. The SEC’s 2026 EDGAR validation suite now checks for semantic consistency at the instance level—meaning identical facts must carry identical values across all tagged locations.

Forensic Threshold: Manual copy-paste workflows between treasury systems and disclosure platforms constitute a control deficiency under SOX Section 404. The PCAOB has noted a 23% increase in material weakness findings related to IT controls between 2020 and 2024.

2026 Disclosure Architecture

API-led connectivity eliminates the Original Quote Gap by maintaining a persistent, queryable link between the ledger cell and the tagged disclosure fact, ensuring data lineage is preserved from origin to submission.

Bridging the Original Quote Gap: The Workiva Wdesk Integration Logic

The Workiva platform functions as the connective tissue between source financial data and SEC-mandated disclosure outputs. Its core technical mechanism—live linking—operates at the cell level. When a treasury datum originates in Finastra’s general ledger and flows into Workiva’s Wdesk environment, it is not imported as a static value. Instead, Workiva establishes a persistent formulaic link between the source dataset and every downstream instance of that data across the reporting ecosystem. A change in a single treasury cell—whether driven by a late-adjusting journal entry, a foreign exchange revaluation, or an intercompany elimination—automatically cascades to every mention across the 10-K, 10-Q, 8-K, proxy statement, and private investor reports.

This linking architecture extends beyond quantitative data points. Narrative disclosures, directional language, and forward-looking statements that reference specific financial thresholds are also bound to the underlying dataset. When the source changes, the narrative updates in parallel, ensuring that qualitative disclosures remain synchronized with quantitative facts. For UHNW entities managing complex multi-entity structures, this eliminates the revision fatigue that traditionally accompanies quarter-end reporting: the “roll forward” process that once consumed days of manual reconciliation is compressed to a single publish action that pushes updated figures to all impacted files simultaneously.

Workiva’s Workiva SEC reporting automation capabilities are further hardened by built-in XBRL and iXBRL tagging infrastructure. The platform incorporates the Arelle open-source validation engine—the same engine used by the SEC for EDGAR validation—plus an additional layer of business-logic checks that examine tagging choices from an accounting perspective. This dual-validation approach reduces the “Tagging Error Risk” that previously plagued private wealth disclosures, where incorrect taxonomy selection or inconsistent fact properties could trigger SEC comment letters or filing suspensions. The platform’s original quote gap financial reporting closure is complete: from the moment data enters the environment, it is linked, tagged, versioned, and audit-trailed through to EDGAR submission.

The UHNW disclosure technology 2026 imperative is clear: entities that rely on traditional ERP modules for disclosure management are forced into manual export-import cycles that break lineage. Workiva’s cloud-native architecture, by contrast, maintains an unbroken chain of custody. Every modification is logged with user attribution, timestamp, and before/after values. External auditors and stakeholders can be granted role-based access to review filings in real time, with tied supporting documents clearly labeled for reference. This transparency transforms the audit from a retrospective forensic reconstruction into a continuous, observable process.

The Finastra Synergy: Feeding the SEC Reporting Engine

If Workiva is the connective tissue, Finastra serves as the Source of Truth. Finastra’s treasury and capital markets platforms—particularly the Summit and Fusion Opics systems—function as the authoritative ledger for complex UHNW financial structures. These systems manage multi-currency positions, cross-border settlements, derivatives valuations, and intercompany balances across jurisdictions. In the 2026 compliance landscape, the integrity of the disclosure is only as strong as the integrity of the ledger that feeds it.

The technical flow from Finastra to Workiva is API-led connectivity in its most rigorous form. Rather than relying on batch-exported CSV files or spreadsheet extracts that must be manually formatted, modern implementations utilize Finastra’s open API architecture to stream structured data directly into Workiva’s datasets. This integration eliminates the need for manual exports entirely. Treasury data—cash positions, investment valuations, liability schedules, and contingent obligation calculations—flows as structured feeds into Workiva, where it is automatically mapped to the appropriate disclosure line items.

For automated SEC filings for family offices, this architecture is transformative. Family offices traditionally operate with lean operational teams where a single controller or CFO may be responsible for consolidating data from multiple custodians, private investment vehicles, and operating companies. The Finastra-to-Workiva pipeline automates the aggregation layer: data from multiple external systems is consolidated within Finastra’s unified ledger, validated for internal consistency, and then synchronized to Workiva as a single source of trusted data. This fintech stack for UHNW 2026 design ensures that the figures appearing in the SEC filing are identical to those recognized by the treasury system—down to the penny, down to the timestamp.

Real-time treasury reporting further compresses the disclosure timeline. Finastra’s Summit platform now incorporates real-time accounting and AI-powered pre-settlement matching, reducing the lag between transaction execution and ledger recognition. When combined with Workiva’s live linking, this means that a transaction executed on a Thursday can be reflected in a draft 10-Q by Friday, with full audit trail and iXBRL tagging intact. For entities facing accelerated filing deadlines or managing investor reporting alongside regulatory obligations, this velocity is not a convenience—it is a competitive and defensive necessity.

Eliminating Revision Fatigue: Version Control in Multi-Entity Audits

UHNW wealth structures are rarely monolithic. They comprise siloed assets across multiple jurisdictions—private operating companies, real estate holding vehicles, investment partnerships, trust structures, and philanthropic entities—each with its own chart of accounts, functional currency, and local regulatory requirements. The challenge of multi-entity compliance technology is not merely aggregating these disparate datasets, but maintaining a unified audit trail that satisfies both SEC auditors and local regulators simultaneously.

Workiva addresses this through hierarchical dataset architecture. Each entity’s financial data resides in its own secured dataset within the platform, with granular permissions controlled down to the cell level. Intercompany eliminations, consolidation entries, and currency translation adjustments are applied as documented transformation layers—each with its own lineage record. When an auditor requests evidence of how a consolidated figure was derived, the platform can expose the complete path: from the subsidiary’s local ledger, through the elimination schedule, through the translation matrix, to the final tagged fact in the iXBRL instance.

This UHNW audit trail automation capability is critical under the SEC’s 2026 scrutiny regime. The EDGAR XBRL Guide explicitly requires semantic consistency: a fact reported as “$10 million” in one location cannot appear as “$11 million” in another within the same submission. In multi-entity environments, such inconsistencies historically arose when different analysts updated different sections of a filing using different versions of a spreadsheet. Workiva’s version control and blackline comparison tools eliminate this risk by enforcing a single, platform-wide source of truth. When a dataset is updated, all linked instances are simultaneously refreshed; when a revision is made, the full history is preserved and comparable across versions.

Version control for SEC filings extends to the XBRL taxonomy itself. Workiva’s historical data roll-forward capability automatically updates prior-period tagged data across files, ensuring that comparative financial statements maintain consistent tagging from quarter to quarter. For UHNW entities with long-dated investment horizons and complex equity structures, this consistency reduces the risk of restatement and the associated legal friction.

Forensic Compliance: Why “Manual” is a 2026 Liability

The SEC’s enforcement posture in 2026 has shifted from forgiving “clerical errors” to treating manual data migration as a presumptive control failure. The Commission’s Inline XBRL mandate was designed specifically to improve data quality and accessibility by embedding machine-readable tags directly into human-readable HTML filings. The underlying premise is that structured data reduces ambiguity—but this benefit is negated when the data feeding the structure has been manually transcribed.

Under SEC data lineage requirements, an auditor must be able to trace any reported figure back to its originating system without encountering undocumented human intervention. When a valuation specialist copies a private equity NAV from a PDF capital account statement into an Excel workbook, then pastes that workbook value into a Word document, then converts that document to HTML for EDGAR submission, the lineage is broken at three distinct points. Each manual transfer introduces the risk of transposition, rounding error, or deliberate manipulation. In 2026, if an auditor cannot trace a figure back to its Original Quote—the first system-of-record instance of that datum—without seeing evidence of human copy-paste intervention, the entity faces a material weakness forensic audit finding.

The risks of manual financial reporting are quantifiable. According to industry analysis, 76% of tax professionals still rely on Excel for calculations in workpapers, and 63% manually gather ERP/GL data. These manual processes create version control issues, disconnected research tools, and fragmented citation tracking that become acute vulnerabilities under audit scrutiny. The IRS has initiated over 100 AI-powered enforcement projects as of early 2026, using machine learning to identify inconsistencies and anomalies in filed data. The SEC is following a similar trajectory: the newly created Cyber and Emerging Technologies Unit has signaled a focus on fraudulent disclosure, indicating a shift toward enforcement actions premised on traditional fraud concepts rather than mere negligence.

2026 compliance audit technology demands that UHNW entities treat their disclosure infrastructure with the same rigor as their trading infrastructure. Just as straight-through processing (STP) eliminated manual settlement risk in capital markets, Zero-Touch Filing eliminates manual disclosure risk. Finastra’s treasury platforms achieve STP rates of up to 90% for settlement workflows; the same discipline must now be applied to regulatory reporting. When data moves from Finastra to Workiva to EDGAR without human transcription, the entity can demonstrate not merely that the numbers are correct, but that they could not have been otherwise.

The “Zero-Touch” Premium: Audit Defensibility as Asset Protection

For UHNW individuals, the value of automated disclosure infrastructure is not measured in hours saved, but in legal friction reduced. In a 2026 forensic audit, having a “digital birth certificate” for every number in a filing—a complete, queryable record of where it originated, who touched it, when it changed, and how it was tagged—reduces the scope, duration, and adversarial intensity of regulatory inquiry. Entities that can produce instant traceability avoid the “fishing expedition” phase of audits, where investigators probe for control weaknesses. The audit becomes a confirmation of known facts rather than a discovery of unknown risks.

This defensibility premium extends to litigation contexts. When a shareholder derivative action or regulatory enforcement proceeding questions the accuracy of a disclosure, the entity with immutable data lineage can demonstrate that its reported figures were not the product of judgment or manipulation, but of synchronized, validated, system-generated data. The Workiva-Finastra stack provides this evidentiary foundation by design.

AI-Tagging Intelligence: The Next Frontier

The final layer of 2026 disclosure automation is AI-assisted iXBRL tagging. Workiva’s platform incorporates machine learning models that predict the correct SEC taxonomy element for a given disclosure, drawing on historical tagging patterns and peer-filing analysis. These models do not replace human judgment—particularly for novel or complex UHNW transactions—but they dramatically reduce the “Tagging Error Risk” that arises from manual taxonomy selection.

The AI engine validates generated tags against the full SEC taxonomy, identifies outliers compared to peer filings in the same industry classification, and flags potential inconsistencies before submission. For UHNW entities with unique asset classes—such as fine art investment vehicles, aircraft leasing structures, or cryptocurrency holdings—this predictive capability ensures that disclosures are tagged with the most granular and accurate available concepts, reducing the likelihood of SEC comment letters requesting additional detail or reclassification.

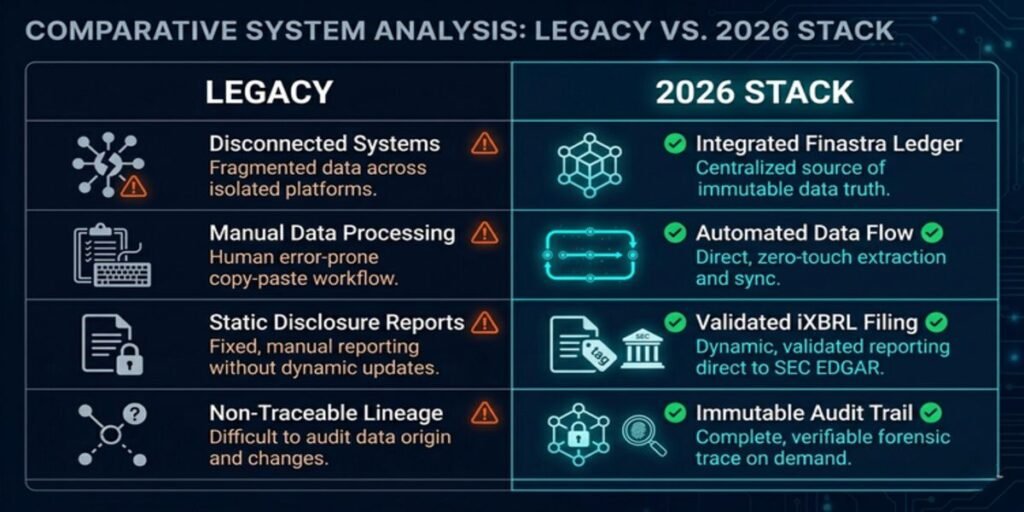

Visual Data Benchmarking: Legacy vs. 2026 Automated Stack

| Feature | Legacy Manual Reporting | 2026 Automated Stack (Workiva/Finastra) |

|---|---|---|

| Data Lineage | Broken (Copy-Paste) | Immutable (API-Linked) |

| Error Risk | High (Human Intervention) | Near-Zero (Source Synchronization) |

| Audit Prep Time | Weeks (Forensic Reconstruction) | Real-Time (Instant Traceability) |

| Regulatory Format | Static PDF/DOCX | Native Inline XBRL (iXBRL) |

| Version Control | Fragmented (Email/Shared Drive) | Centralized (Platform-Native) |

| SOX Control Evidence | Retrospective Documentation | Continuous Operational Byproduct |

Forensic Intelligence: Frequently Asked Questions about SEC Disclosure Technology

Q1: What is the Original Quote Gap in SEC reporting?

The Original Quote Gap is the forensic vulnerability that occurs when source data from a system of record—such as a general ledger or treasury platform—is manually extracted and re-entered into a disclosure document. This severs the digital audit trail. In 2026, if an auditor cannot trace a figure directly from an EDGAR filing back to its source without encountering a human copy-paste intervention, the entity faces a material weakness finding. Closing this gap requires API-led connectivity to ensure data flows through automated, validated pipelines.

Q2: Why do UHNW entities prefer Workiva over traditional ERP modules?

Traditional ERPs focus on operational accounting, whereas Workiva is architected for the “last mile” of regulatory narrative. It provides granular linking technology that binds a single data point to multiple locations, collaborative workflow for multi-party review, and a native iXBRL tagging engine. For complex UHNW structures spanning multiple jurisdictions, Workiva’s ability to consolidate and version-control disparate datasets within a unified, audit-trailed environment is operationally indispensable.

Q3: How does Finastra automate 2026 regulatory compliance?

Finastra’s platforms (Summit/Fusion Opics) serve as the authoritative ledger for complex financial operations. Through open API architecture, Finastra streams structured data directly into Workiva, eliminating manual import cycles that introduce latency. This means data recognized in the ledger is available for disclosure tagging within minutes, with the full transformation logic preserved. Finastra also continuously updates its modules to reflect evolving SEC, EMIR, and MiFIR requirements, ensuring data is compliance-validated at the source.