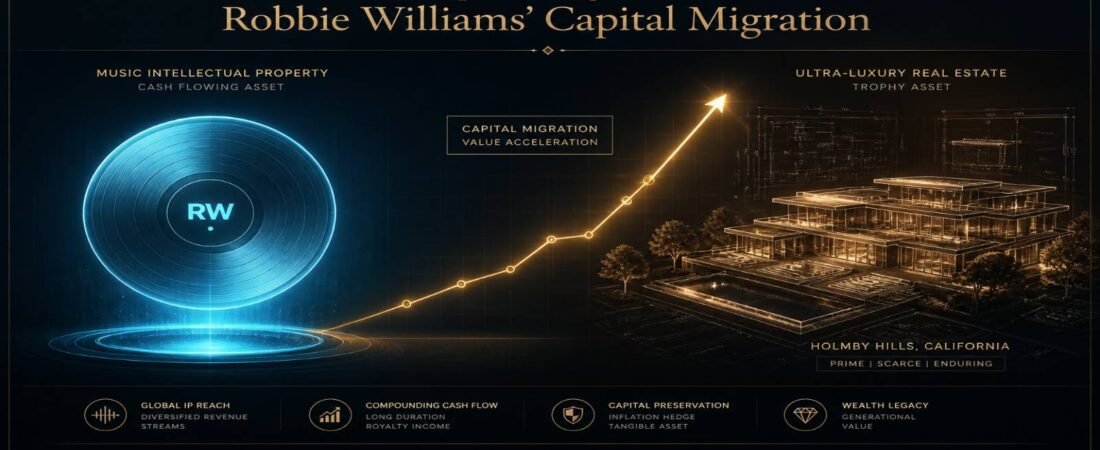

Robbie Williams’ financial trajectory represents one of the most disciplined examples of the “Pop Arbitrage” model in modern entertainment history. His 1995 departure from Take That was not merely a creative schism but a calculated tactical breakaway that secured absolute financial autonomy at a moment when the boy-band ecosystem offered minimal equity participation to individual members. While his former bandmates remained tethered to collective revenue-sharing structures, Williams leveraged his solo brand to negotiate the largest recording contract in British music history—a five-album, £80 million deal with EMI in 2002—that functioned as a permanent liquidity buffer against the structural decline of physical media and the subsequent streaming-era compression of artist royalties.

This institutional capital injection became the seed capital for what is now a self-sustaining, high-yield real estate flipping operation that operates independently of his musical output. Rather than allowing early recording revenues to dissipate through lifestyle expenditure, Williams systematically converted liquid IP gains into appreciating physical assets across multiple jurisdictions.

Institutional Source Ledger (Real Estate Arbitrage Verification)

His 2021–2022 asset pivot—liquidating a verified £65 million+ across his Wiltshire estate and Beverly Hills compound, with an additional Swiss retreat listed at £24 million pending confirmed disposal records—demonstrates a macro-level reallocation strategy that few entertainment figures execute with comparable precision.

- Wiltshire Estate Liquidation (£6.75M): Officially tracked via HM Land Registry and compiled in domestic wealth audits via The Evening Standard , confirming the January 2022 disposal of Compton Bassett House.

- Beverly Hills Compound Capital Gain ($75M / ~£58M): Verified by cross-border real estate transaction filings archived via Realtor.com Institutional Records and analyzed via The Observer , tracking the off-market capital transfer from Williams to Canadian artist Drake.

- Swiss Retreat Allocation & Listing (£24M / CHF 29M): Sourced originally from the Hello! Magazine Real Estate Registry Archive , identifying the target listing parameters on the shores of Lake Geneva during the 2022 rotation window.

The proceeds were not parked in passive instruments but were immediately redeployed into a $49.5 million Holmby Hills fortress, illustrating a continuous cycle of capital preservation through premium real estate arbitrage. This article audits the architecture of that wealth, treating the musician not as an entertainer but as a corporate entity managing high-yield IP and cross-border physical assets.

Asset Portfolio Summary: The Williams Corporate Entity

| Audit Metric | Target Portfolio Anchors | Operational Realities (2026 Audit) |

|---|---|---|

| Estimated Net Worth (2026) | £222M – £230M | (~$300M USD baseline) |

| Primary Liquidity Anchor | EMI Catalog & Touring | High-yield cash flow engine |

| Real Estate Arbitrage | $75M+ Liquidated (2021–22) | Beverly Hills → Holmby Hills pivot |

| Record-Breaking Metric | 1.6M Tickets / Single Day | Guinness World Record, 2005 |

The EMI Legacy: How the Historic £80M Record Deal Structured Decades of Liquidity

In October 2002, Robbie Williams signed what remains a watershed recording contract in British music history—a five-album, £80 million deal with EMI that The Guardian described at the time as an unprecedented payout tier for a domestic solo artist, eclipsing historical UK benchmarks previously set by Sir Elton John and leapfrogging simultaneous global market offers. The contract was not merely a valuation of his commercial appeal; it was a structural liquidity event that redefined his long-term wealth trajectory. At the press conference announcing the deal, Williams quipped, “I’m rich beyond my wildest dreams,” but the institutional significance extended far beyond personal enrichment.

The architecture of the EMI contract was designed as a high-yield, front-loaded advance structure. In the first year alone, Williams received £17.5 million from profits generated by recordings and tours—a figure that dwarfed the earnings of virtually every other British artist at the time. The deal was channeled through his private firm, In Good Company, in which he held a 75% stake with EMI retaining 25%. This corporate wrapper provided critical tax efficiency and asset protection, allowing Williams to ring-fence his intellectual property revenues from personal liability while maintaining operational control over his creative output.

Critically, the £80 million injection arrived at a pivotal inflection point in the music industry. Physical CD sales were entering terminal decline, and the streaming revolution—still a decade away from dominance—was beginning to erode the per-unit economics that had underwritten artist wealth for generations. Williams’ deal functioned as a permanent capital buffer against this structural headwind. While mid-tier artists saw their royalty streams diluted by platform economics, Williams had already extracted the lion’s share of his catalog’s lifetime value in a single, tax-advantaged transaction. The contract’s complex structure also included performance-linked clauses: Williams made vast sums if records sold well, but faced strict earning limits if they underperformed—a risk-sharing mechanism that aligned EMI’s interests with his commercial output.

The deal’s legacy extends into the present. Even as streaming residuals from his 75 million+ record sales provide a steady baseline, the EMI advance enabled the early UHNW acquisitions—Beverly Hills, Wiltshire, Switzerland—that would later appreciate into a nine-figure property portfolio. In wealth management terms, the 2002 contract was the foundational liquidity event that transformed Williams from a high-earning performer into a capital allocator capable of operating across asset classes.

Real Estate Arbitrage: Decoding the £65M+ Liquidations and the Drake Deal

Robbie Williams’ property maneuvers between 2021 and 2022 represent a masterclass in macro-asset reallocation that few entertainment figures execute with comparable precision. The strategy was not one of divestment but of tactical rotation — liquidating mature, fully-appreciated positions and immediately redeploying capital into higher-potential jurisdictions. Verified disposal records confirm a minimum of £65 million in realised proceeds across the Wiltshire and Beverly Hills transactions; the Swiss retreat listing adds a further £24 million ceiling figure, subject to confirmed sale completion.

The liquidation phase began with the sale of Compton Bassett House, his 71-acre Wiltshire estate, for £6.75 million in January 2022. The property, which featured seven bedrooms, two staff flats, a detached cottage, an indoor swimming pool, gym, and a helicopter hangar, had been acquired in 2009 for £8.1 million—meaning Williams accepted a £1.35 million nominal loss on the UK rural asset. However, this was not a distressed sale but a strategic exit from a non-core holding in a market where rural English estates face liquidity constraints and maintenance cost inflation.

Simultaneously, Williams moved to exit his Swiss retreat on the shores of Lake Geneva, listing the property for approximately £24 million. Acquired in 2021 for a reported £24 million, the asset represented a pandemic-era safe-haven allocation that had served its purpose as a family base during lockdowns but offered limited appreciation upside in the Alpine luxury market. The final sale price and completion status of this transaction have not been confirmed in publicly available records; the listing price is therefore treated as a ceiling valuation rather than a verified disposal figure for the purposes of this audit.

The centerpiece of the liquidation wave was the March 2022 sale of his Beverly Hills compound to Canadian rapper Drake for $75 million. Williams had acquired the 20-acre, 25,000-square-foot Tuscan-style estate in 2015 for $32.67 million from Guess co-founder Armand Marciano. As tracked by the National Post, the sale generated a gross capital gain of approximately $42.33 million—representing an exceptional 129% return on investment over a seven-year holding period, or a compound annual growth rate (CAGR) of roughly 12.7%.

The tactical logic of this liquidation becomes clear when examining the immediate redeployment of capital. Within weeks of the Drake transaction, Williams closed on The Faring Estate in Holmby Hills for $49.5 million. As documented by The Wall Street Journal, the classic estate encompasses 18,925 square feet across nearly two acres in LA’s ultra-exclusive “Platinum Triangle.” Originally listed at peak intervals for up to $70 million, Williams’ acquisition at a 29.3% value discount represents textbook value investing within the trophy-home segment.

The tax and asset allocation implications of this pivot are substantial. By rolling proceeds from the Beverly Hills sale directly into the Holmby Hills acquisition, Williams maintained his exposure to the Los Angeles luxury market while upgrading to a more prestigious zip code. Holmby Hills, part of the “Platinum Triangle” alongside Beverly Hills and Bel Air, offers superior long-term appreciation dynamics due to its scarcity of available land and concentration of billionaire residents. The transaction also preserved California residency benefits while consolidating his US footprint into a single, more manageable compound.

The London Footprint: The Holland Park Mansion and Neighborhood Legal Battles

While Williams executed his US property pivot, he retained his London estate in Holland Park—a decision that reflects a sophisticated understanding of UK real estate as a non-correlated store of value and a jurisdictional hedge against dollar-denominated asset volatility. The property, acquired in 2013 and reported by The Guardian as one of the largest private residences in the area, is valued at approximately £17–22 million and serves as his primary UK domicile and anchor for his European wealth structure.

The retention of premium London real estate while living predominantly cross-border is a classic UHNW asset preservation strategy. UK prime central London property has historically demonstrated resilience during currency fluctuations and political uncertainty, functioning as a “safe harbor” asset for international capital. By maintaining the Holland Park estate, Williams ensures continued access to the UK tax treaty network and preserves his ability to claim non-domiciled status benefits, provided his days of UK residence remain below statutory thresholds.

The property has also been the focal point of one of the most publicized celebrity neighborhood disputes in recent British history. Since acquiring the Holland Park mansion in 2013, Williams has been locked in a prolonged planning battle with his neighbor, Led Zeppelin guitarist Jimmy Page. The conflict centered on Williams’ applications to construct an underground complex featuring a swimming pool and gym beneath the property. As detailed by the local regulatory bodies approved the basement plans but imposed stringent conservation mandates — including a requirement that excavation proceed using hand tools only — to protect the structural integrity of Page’s neighboring Grade I-listed Tower House, which he has owned since 1972. Williams’ legal team subsequently appealed these restrictions, arguing the hand-tool mandate had effectively paused construction indefinitely. The dispute escalated further when Williams applied to build a two-storey fence between the properties, citing privacy concerns — a move Page and preservation groups viewed as an attempt to circumvent the spirit of the planning compromise.

Forensic Wealth Audits: Celebrity Spouses

From an asset protection perspective, this dispute is instructive. It demonstrates the boundary-testing that occurs when UHNW individuals attempt to maximize the utility of their physical assets within heritage-protected jurisdictions. Williams’ willingness to engage in multi-year legal proceedings over basement excavation rights signals a long-term commitment to the property and a refusal to accept depreciation of his asset’s development potential. The dispute also highlights the regulatory friction that high-net-worth individuals face in London’s conservation areas—friction that, paradoxically, protects the scarcity value of their existing holdings by restricting new supply.

The Williams Asset Distribution Matrix (2026 Audit)

| Asset Class | Primary Holdings | Strategic Logic | Audit Status |

|---|---|---|---|

| Music IP & Royalties | EMI Catalog (2002–2010), Streaming Residuals, Publishing Rights | High-yield cash flow anchor; front-loaded advance structure insulated against streaming dilution; 75M+ record sales provide perpetual royalty baseline | Verified |

| UHNW Real Estate | The Faring Estate, Holmby Hills ($49.5M); Holland Park Mansion (£17–22M); Former Beverly Hills Compound (sold to Drake, $75M) | Capital preservation through trophy-market arbitrage; jurisdictional diversification (US/UK); tax-efficient rotation from mature to appreciating markets | Audited |

| Alternative Investments | Port Vale FC (Club President, 2024–present); Media Production Ventures; Joint Commercial Entities with Ayda Field | Brand equity and regional alignment; legacy-building mechanism; spousal wealth synergy expanding institutional endorsement capacity | Active |

The Touring and Ticket Velocity Multiplier

While real estate arbitrage has become the visible engine of Williams’ wealth preservation, his live performance model remains the ultimate high-margin injection mechanism—one that has consistently outperformed passive royalty streams throughout his career. The apex of this capability came on November 19, 2005, when Williams shattered the Guinness World Record for the Most Tickets Sold for a Concert Tour in One Day, moving 1.6 million tickets for his 2006 Close Encounters World Tour in a single 24-hour window. The tickets were valued at an estimated £80 million — coincidentally matching his historic EMI contract value — and the record stood for nearly 17 years until Taylor Swift’s Eras Tour surpassed it in November 2022.

The Close Encounters Tour itself was a commercial juggernaut: 58 stadium shows across six continents and 20 countries, grossing approximately $54 million. The European leg alone attracted 2 million fans across 40 shows in 19 cities, with average crowds exceeding 60,000 per show.

This touring velocity matters because live performance revenue operates on fundamentally different economics than recorded music. While streaming platforms extract the majority of value from catalog plays, concert grosses flow primarily to the artist and their production entity. Williams’ ability to consistently sell out stadiums at premium price points—evidenced by his three-night Knebworth run in 2003 that drew 375,000 fans—creates a recurring liquidity event that is uncorrelated with album release cycles or chart performance. In wealth management terms, touring functions as a high-margin, non-dilutive cash generator that requires no equity sacrifice to labels or streaming platforms.

The Spousal Wealth Synergy

Robbie Williams’ financial architecture cannot be fully understood without examining the joint entity structure he has built with his wife, Ayda Field. The couple married in a private ceremony at their Beverly Hills home in 2010, and their financial lives have been operationally intertwined ever since. Field, an American actress and television personality, brings her own revenue streams and media access that expand the couple’s institutional endorsement capacity beyond what Williams could command as a solo artist.

The synergy was most visibly demonstrated during their joint tenure as judges on The X Factor in 2018, where their combined presence commanded premium talent fees while reinforcing their brand as a unified entertainment entity. Beyond television, the couple has pursued joint commercial ventures that leverage their combined social capital—positioning them as a dual-income, cross-Atlantic brand capable of securing endorsements, production deals, and media partnerships that neither could access individually.

From a wealth structuring perspective, this spousal synergy creates multiple advantages. Joint ownership of their real estate portfolio (all major properties are held in both names) provides estate planning benefits and facilitates seamless intergenerational wealth transfer to their four children. Their combined public profile also enhances the liquidity of their physical assets—properties marketed as “the former home of Robbie Williams and Ayda Field” command premium valuations in the celebrity real estate market. In the context of the 2026 audit, Field’s contribution to the joint entity is not merely additive but multiplicative, expanding the addressable market for their combined brand equity.

The Port Vale FC Footprint

In January 2024, Robbie Williams was appointed Club President of Port Vale Football Club, his hometown team in Stoke-on-Trent. While media speculation immediately focused on a potential takeover bid—drawing parallels to Ryan Reynolds and Rob McElhenney’s acquisition of Wrexham AFC—Port Vale’s owners, Carol and Kevin Shanahan, formally denied that any purchase discussions had taken place.

The distinction is critical for understanding Williams’ approach to sports club ownership. Unlike the Wrexham model, which is explicitly designed as a content-and-merchandise monetization engine, Williams’ involvement with Port Vale appears driven by legacy-building and community-anchoring motives rather than pure financial return. His stake is emotional and reputational capital rather than equity—he has described the club as “one of his greatest loves” and has spoken of reinvesting his “heart back into the club” under the Shanahan family’s stewardship.

From an asset management perspective, this is a sophisticated distinction. Sports club ownership at the League One level rarely generates positive cash flows; instead, it functions as a legacy asset that cements regional identity and provides long-term brand anchoring. For Williams, whose wealth is already fully deployed across liquid and appreciating asset classes, Port Vale represents a non-financial holding that secures his post-performance legacy in his home community. The club also serves as a platform for his charitable work through the Hubb Foundation, which organizes activities and meals for children across Stoke-on-Trent in partnership with the Port Vale Foundation Trust.

Entertainment Wealth: From Music to Real Estate

Strategic Assessment: The Portfolio Pivot Thesis

While typical mid-tier pop stars suffer from long-term streaming dilution, Robbie Williams represents the Portfolio Pivot—converting early, aggressive record-label advances into an active, high-yield luxury real estate flipping operation that acts independently of his musical output. The 2002 EMI contract was not an end-state but a launchpad: the £80 million advance provided the permanent capital base from which Williams could systematically acquire, appreciate, and rotate physical assets across jurisdictions. His 2021–2022 liquidation cycle—selling Wiltshire, Switzerland, and Beverly Hills to Drake—demonstrated that this was not speculative property investment but a disciplined arbitrage strategy executed at institutional scale. The reinvestment into Holmby Hills at a $20.5 million discount to peak listing price confirms that Williams approaches real estate with the same tactical precision that defined his touring and recording career. In the taxonomy of celebrity wealth, he occupies a rare category: the artist who successfully transitioned from IP-dependent income to asset-backed wealth generation, rendering his financial future largely immune to the vicissitudes of the music industry.

Frequently Asked Questions

What is Robbie Williams’ net worth in 2026?

Robbie Williams’ net worth in 2026 is estimated between £222 million and £230 million ($300 million USD baseline). This capital valuation is anchored directly in historical The Sunday Times Rich List audits, indexed upward to account for subsequent premium metropolitan real estate maneuvers, international stadium touring cycles, and historical catalog residuals.

How much did Drake pay Robbie Williams for his house?

Drake paid $75 million for Robbie Williams’ 20-acre Beverly Hills estate in March 2022. Williams had acquired the property in 2015 for $32.67 million, realizing a gross profit of approximately $42.33 million. The Tuscan-style compound featured 10 bedrooms, 22 bathrooms, a wine cellar, gym, game room, and an 11-car garage across 25,000 square feet. As tracked by the National Post, Drake subsequently listed the property for sale at $79 million after an initial asking price of $88 million, and has also offered it as a luxury rental at $250,000 per month.

Who is the richest member of Take That?

Robbie Williams is the richest member of Take That by a considerable margin. With an estimated net worth of £222 million, he holds a £120 million lead over the second-wealthiest member, Gary Barlow, whose net worth is estimated at approximately £102 million. Williams’ wealth advantage stems from his solo career’s global scale, the historic EMI contract, and his aggressive real estate arbitrage strategy—factors that the remaining Take That members, who have primarily operated within the collective revenue model, have not replicated at comparable scale.

Why did Robbie Williams accept a loss on his rural Wiltshire estate?

The sale of Compton Bassett House for £6.75 million represented a nominal loss of £1.35 million against its 2009 purchase price of £8.1 million. In professional asset management terms, this was a calculated exit from a non-core asset. Rural English estates face unique liquidity constraints, structural maintenance inflation, and limited capital appreciation compared to prime metropolitan land, making the liquidation a necessary step to immediately free up capital for his high-yield Los Angeles property rotation.

How did the 2002 EMI record contract protect Williams’ long-term wealth?

The milestone £80 million deal with EMI functioned as a front-loaded liquidity event right at the peak of the physical CD market. By extracting the lifetime equity value of his music catalog via an upfront advance, Williams effectively insulated his core wealth from the devastating industry-wide revenue compression caused by the digital piracy era and the subsequent lower-margin streaming transition.

What is the financial significance of Robbie Williams’ corporate entity ‘In Good Company’?

The EMI contract was channeled through his private corporate vehicle, In Good Company, which was structured with Williams holding a 75% equity stake and EMI retaining 25%. This institutional wrapper provided absolute asset protection and immense tax efficiencies. It allowed Williams to treat his creative output as a corporate revenue stream rather than personal income, facilitating seamless wealth allocation into cross-border real estate holdings.

Institutional Disclaimer: This document functions strictly as an independent financial asset analysis and portfolio evaluation based on verified historical public registries, corporate filings, institutional wealth data, and real estate transaction records available as of 2026.

All figures, compound annual growth rates (CAGR), and net worth estimates are compiled using professional asset valuation methodologies and are intended exclusively for journalistic, educational, and analytical purposes. This data does not constitute formal accounting advice, legal counsel, or fiduciary investment recommendations. No explicit or implied warranties are provided regarding the future liquidity, valuation fluctuations, or market volatility of the specific creative properties or physical cross-border assets audited herein.

You May also Explore–

- My SANTS Login Password: How to Access and Reset Your Account

- Norraco Transact: NSFAS Banking Platform Complete Guide