Kunal Shah operates not merely as an angel investor, but as a decentralized venture capital institution. With 354 recorded investments and 68 exits, the CRED founder has constructed India’s highest-density startup portfolio, deploying capital at a velocity that rivals traditional seed funds. His strategy transcends conventional angel investing—he isn’t buying equity; he’s purchasing high-fidelity intelligence access across the global technology ecosystem. By deploying modest $10,000-$50,000 checks at unprecedented scale, Shah has built a distributed R&D network that feeds real-time market intelligence back to his primary operating company while maintaining optionality on India’s next generation of unicorns.

This forensic audit examines the architecture of Shah’s syndicate: the “frictionless capital” model that attracts founders, the fintech-AI convergence driving his 2026 deployment, and the power-law mathematics that make a 20% write-off rate not merely acceptable, but optimal. For family offices and limited partners evaluating operator-investor models, Shah’s portfolio represents a masterclass in network-driven venture deployment.

The “Unicorn Density” Strategy: A Masterclass in Seed-Stage Capital

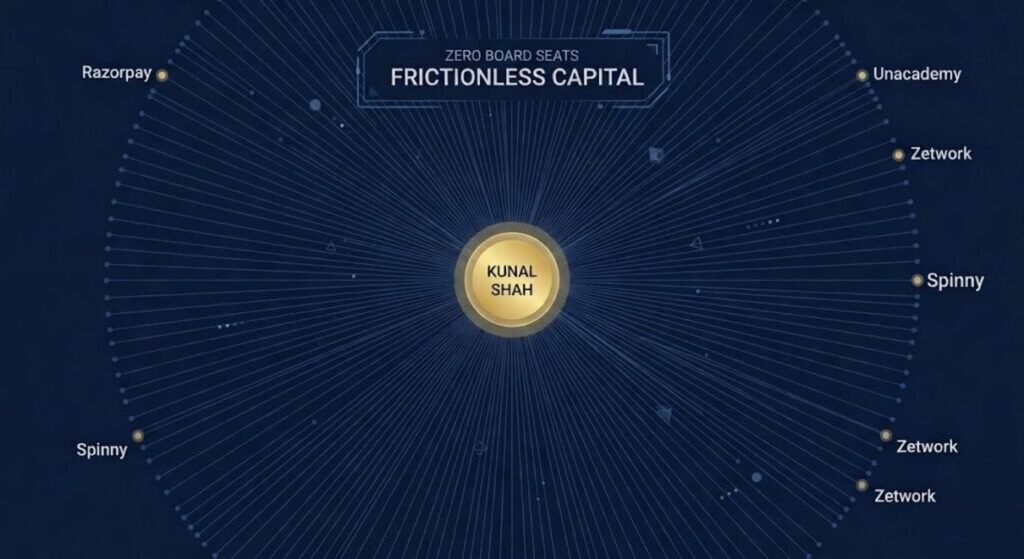

Shah’s investment philosophy diverges fundamentally from traditional venture capital. While institutional VC firms concentrate capital into 15-20 portfolio companies and demand governance rights through board seats, Shah operates on radical diversification—deploying 354 investments with a “frictionless capital” approach that deliberately avoids operational interference. Kunal Shah invests between $10,000 and $50,000 per startup, typically letting founders determine the exact amount, creating a low-friction entry point that attracts top-tier founders who need capital without complexity.

This density creates compound network effects. As one portfolio founder noted, “Kunal does one deal a day. He gets the quality of deal flow that would make the best VCs jealous.” His deal flow originates from a self-reinforcing ecosystem: repeat entrepreneurs, senior startup executives, Sequoia Capital and Ribbit Capital (his own investors), and a growing cadre of portfolio founders who refer subsequent deals. Each investment strengthens the flywheel, creating a proprietary intelligence network that traditional funds cannot replicate.

The founder preference for Shah’s capital stems from what we term the “Zero-Disclosure Advantage.” Unlike institutional VCs who require board seats, detailed reporting, and governance oversight, Shah provides capital with minimal operational friction. Founders gain the signaling value of his name on their cap table—often sufficient to attract subsequent funding rounds—without surrendering strategic autonomy. This “high-signal, low-friction” model explains why Shah has funded over 266 startups including Razorpay, Snapdeal, Zetwork, BlueSmart, Unacademy, and Spinny, with 11 achieving unicorn status according to Tracxn data.

From Transaction to Intelligence: The Fintech-AI Convergence

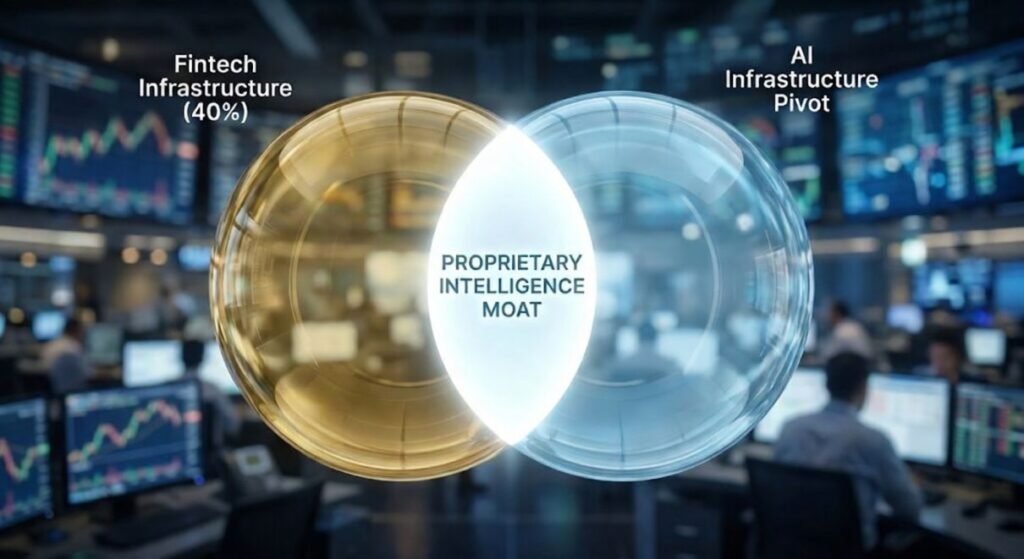

Shah’s asset allocation reveals a sophisticated sector thesis. Approximately 40% of his investments target consumer tech, including D2C brands like Mensa Brands and BharatX, while 89 bets focus specifically on fintech innovations—neobanking, BNPL, and payments infrastructure. This concentration reflects his operator expertise from building Freecharge and CRED, creating what we term “domain alpha” in fintech selection.

The 2026 pivot into AI infrastructure represents the next evolution of this thesis. Shah recently backed HRtech startup Presentations.AI and analytics firm Revrag.ai, alongside US-based AI risk management company SydeLabs. This AI allocation isn’t speculative—it’s defensive positioning. Shah has publicly stated that the cost of coding has dropped significantly due to AI and will dramatically drop further, predicting that professionals who effectively use AI tools will become 2-3x more productive. His AI investments function as hedges against this disruption while capturing upside from the infrastructure layer that will enable it.

The intelligence network thesis underpins this allocation. Shah’s 354 investments function as a distributed R&D department, providing real-time data on market shifts, consumer behavior changes, and emerging technology adoption curves. When Razorpay co-founder Harshil Mathur consults Shah before each funding round to determine investor selection and stake allocation, he’s accessing not just capital but high-fidelity market intelligence. This cap-table access provides Shah with proprietary data on fintech infrastructure needs, payment flow patterns, and credit market dynamics that directly inform CRED’s product roadmap.

Liquidity Velocity: Deconstructing the Capital Recycle Loop

The sustainability of Shah’s high-volume model depends on systematic liquidity management. With 68 recorded exits from 354 investments according to PitchBook data, Shah maintains a 19% exit rate that funds continuous deployment without requiring external LP capital. This “capital recycle loop” operates through multiple liquidity mechanisms.

Early-stage angel investments typically achieve liquidity through three channels: acquisition by strategic buyers, IPOs of mature portfolio companies, and secondary sales to later-stage venture funds. While Shah’s personal secondary transactions remain private, the 68 exit events demonstrate systematic portfolio pruning. High-performing early stakes in companies like Razorpay (now valued at $7.5 billion+), Unacademy (valued at $3.13 billion at peak), and Spinny (used-car marketplace unicorn) provide the liquidity events necessary to recycle capital into new seed-stage opportunities.

This velocity model contrasts sharply with traditional VC fund lifecycles. While institutional funds operate on 10-year horizons with rigid deployment schedules, Shah’s personal capital allows continuous recycling. An early $25,000 stake in a seed-stage fintech that achieves Series C valuation can return 10-20x through secondary sale to growth-stage investors, funding 20-40 subsequent seed checks. This “liquidity bridge” strategy enables perpetual deployment without the capital constraints that limit traditional angel investors.

The “Anti-Portfolio” & Write-Offs: Friction in the High-Volume Model

Institutional objectivity requires acknowledging the portfolio’s friction points. The 2024-2025 edtech correction exposed vulnerabilities in Shah’s high-volume approach. Unacademy, despite achieving unicorn status and raising $440 million in Series H funding at a $3.13 billion valuation, reported losses of ₹1,678 crore in FY23 as post-COVID demand normalization disrupted the online education market. Similarly, Vedantu and other edtech holdings faced comparable pressure as customer acquisition costs spiked and unit economics deteriorated following the return to physical classrooms.

However, in power-law venture mathematics, a 20% write-off rate is a feature, not a bug. Seed-stage investing operates on the principle that a single unicorn return can offset 50-100 total losses. Shah’s 11 unicorn hits from 354 investments (3.1% hit rate) significantly exceeds venture industry averages. The edtech write-offs, while material in absolute terms, represent acceptable casualties in a portfolio construction model optimized for asymmetric upside.

The anti-portfolio—companies Shah passed on or that failed after investment—includes the typical carnage of early-stage venture. Yet the density of his deployment ensures that even sector-specific corrections (edtech, certain consumer D2C brands) cannot destabilize the overall portfolio architecture. With 354 positions, no single write-off can create catastrophic loss, while the 68 realized exits provide continuous liquidity to maintain deployment velocity regardless of sector-specific downturns.

Institutional Intelligence: Elite Assets & Legacies

Kunal Shah Net Worth 2026: Paper Wealth vs. Liquidity Velocity

As of Q1 2026, Kunal Shah’s net worth is estimated at approximately $2.0 Billion (₹15,000 Crore). However, a forensic look at his balance sheet reveals a sophisticated “Two-Tier” wealth structure. Unlike traditional billionaires whose wealth is tied to a single public entity, Shah’s net worth is a hybrid of his majority stake in CRED and a highly liquid, decentralized angel syndicate.

The CRED Equity Anchor (Paper Wealth): The primary driver of Shah’s paper wealth is his ownership in Dreamplug Technologies (CRED). Following the market corrections of 2025, CRED’s valuation stabilized at $3.5 Billion, down from its $6.4 Billion peak. While this “down-round” adjusted his marked-to-market net worth, Shah’s refusal to take a traditional executive salary—maintaining a symbolic ₹15,000 per month—signals a “Long-Equity” conviction.

The Angel Syndicate (Liquid Alpha): The most underestimated component of Shah’s wealth is the Liquidity Velocity of his 354-company portfolio. While most of his $2 billion net worth is “locked” in CRED equity, Shah has mastered the Secondary Recycle Loop. By systematically selling early-stage “Angel” stakes in companies like Razorpay and Spinny to growth-stage VC firms, Shah generates significant private liquidity to fund 50–60 new seed checks annually.