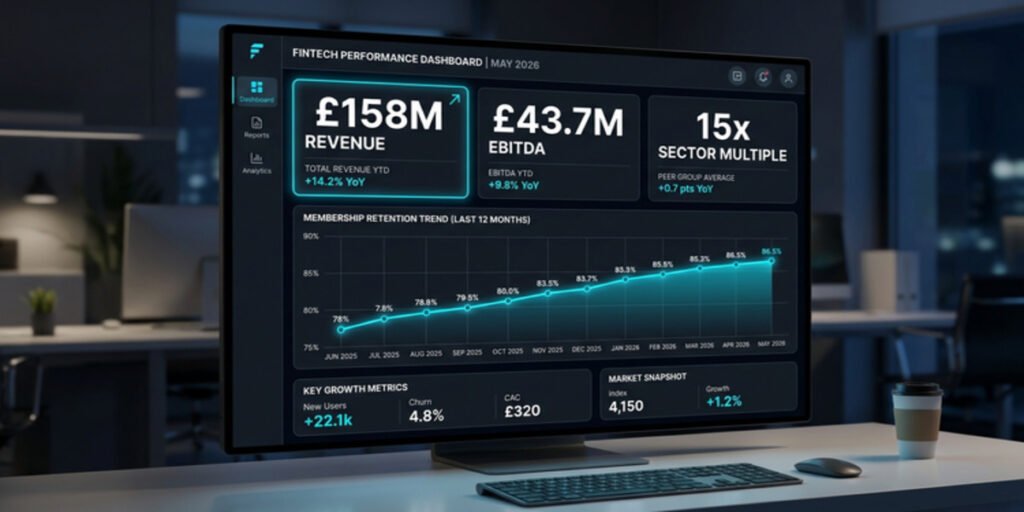

The April 2026 financial filing for Bannatyne Group marks the clearest evidence yet that Duncan Bannatyne’s post-divorce rebuilding strategy has worked. A thirteen-year operational rehabilitation has transformed a stripped-back asset base into a cash-generative wellness business that now outperforms both discretionary retail and budget fitness chains during macroeconomic compression. With record turnover of £158 million for the year ending December 2025, operating profits of £27.2 million, and EBITDA holding steady at £43.7 million, the 2026 fiscal year is not merely a recovery milestone; it is a validation of the ‘Phoenix Recovery’ thesis for UHNW individuals who have rebuilt through operational excellence rather than speculative leverage.

The 2026 fiscal year is not merely a recovery milestone; it is a validation of the “Phoenix Recovery” thesis for Ultra-High-Net-Worth individuals who have rebuilt through operational excellence rather than speculative leverage.

This audit frames Bannatyne’s trajectory as a blueprint for UHNW asset reconstruction. The 2013 divorce from Joanne McCue functioned as a forced “reset point” that stripped away the speculative periphery—film investments, leveraged property plays, and media-centric diversification—leaving only the cash-generating core of 70 locations, 219,743 active members, and an integrated spa-hotel ecosystem. Where the 2006-era Bannatyne empire was built on aggressive debt-funded acquisition (most notably the £92 million Hilton health club purchase and a £180 million Anglo Irish Bank facility), the 2026 model is defined by capital discipline, margin protection, and strategic utilization of existing real estate through the high-margin padel court rollout. The result is a personal net worth that industry trackers now place between £480 million and £515 million, with the underlying enterprise value likely exceeding £700 million when premium wellness EBITDA multiples are applied.

Bannatyne Asset Matrix: 2026 Valuation Estimates

The Divorce Decimation: How the 2013 Settlement Redefined the Bannatyne Asset Baseline

The forensic impact of Duncan Bannatyne’s 2013 divorce from Joanne McCue remains one of the most instructive case studies in UK High-Net-Worth legal risk. The dissolution of their seven-year marriage—initiated by a text message received while Bannatyne was filming Dragons’ Den at Pinewood Studios—triggered an asset transfer that contemporaneous reports and Bannatyne’s own public statements valued at approximately £345 million, though the precise figure has never been confirmed by either party. Bannatyne himself acknowledged in a 2013 interview with The Scotsman that his published wealth had collapsed from £430 million to approximately £85 million, a figure that implied the loss of roughly 80% of his stated net worth through the settlement, legal costs, and concurrent asset devaluation.

The settlement’s structural damage extended far beyond personal liquidity. Bannatyne was forced to sell his luxurious villa on the French Riviera and retrench to a more modest property on Lake Windermere. More critically, the divorce coincided with the legacy of a £180 million Anglo Irish Bank facility drawn in 2006, which funded the £92 million Hilton acquisition and broader estate expansion—just before the bank’s collapse during the global financial crisis.

The confluence of marital asset division and frozen credit lines necessitated a fundamental strategic pivot: Bannatyne could no longer fund growth through leveraged acquisition. Instead, he was compelled to extract maximum yield from existing operational assets, transitioning from a speculative, debt-funded expansion model to one governed by operating cash flow discipline. This transition, painful as it was, laid the groundwork for the EBITDA-stable empire that exists today.

From a legal-risk perspective, the Bannatyne-McCue dissolution is now cited in family law circles as a masterclass in why late-in-life marriages require forensic asset disclosure and pre-nuptial structuring. Bannatyne has publicly stated that his best man advised a pre-nuptial agreement but he dismissed it as “unromantic”—a decision he has since described as his most costly business error. The case also illustrates the danger of interim payment demands during proceedings; McCue reportedly sought £1,000 per day as an interim award, while Bannatyne was forced to make staff redundancies to manage cash flow.

For UHNW entrepreneurs, the lesson is stark: emotional decisions about marital contracts carry direct enterprise consequences. The Duncan Bannatyne divorce settlement impact was not merely a personal tragedy but a forced operational restructuring that eliminated speculative risk from the corporate balance sheet and replaced it with the high-yield, membership-driven model that now defines the group.

The Membership Multiplier: Decoding the £158M Revenue Engine of The Bannatyne Group

The Bannatyne Group annual report 2026 (covering the fiscal year ending December 2025) reveals a business that has achieved what few UK hospitality operators have managed: genuine top-line growth against a backdrop of significant cost inflation — driven in part by employer National Insurance increases that Bannatyne has publicly criticised as a policy failure. Revenue reached £158 million, up 6% from £149.6 million in 2024, while operating profits climbed to £27.2 million (from £25.8 million) and EBITDA held firm at £43.7 million. Pre-tax profits rose to £15.7 million from £14.4 million. These figures are particularly notable given that the group absorbed a £2 million increase in employer National Insurance contributions and faces energy tariffs that now represent 11% of the total cost base. The membership count—219,743 active members, up from 219,500—demonstrates that retention rates in the premium mid-market segment remain robust even as disposable income contracts.

The valuation logic underpinning these numbers is critical for investors analyzing fitness industry EBITDA multiples in the 2026 private equity market. While volume-based operators trade at compressed multiples due to churn and price-war vulnerability, Bannatyne’s integrated “health club + spa + hotel” ecosystem commands premium valuation. The recurring revenue model—annual memberships paid via direct debit, supplemented by spa day passes, hotel stays, and ancillary personal training—generates predictable cash flows that PE firms now value at 12–18x EBITDA.

This is in stark contrast to the 6–8x multiples typical of transactional gym models. While Mike Ashley (Frasers Group) represents the volume-based fitness play, Duncan Bannatyne represents the Premium Mid-Market Pivot—leveraging brand loyalty and spa-integration to maintain higher ARPU (Average Revenue Per User). The UK health club market share data supports this: Bannatyne Group remains the largest independent chain, and its 70-site footprint provides geographic diversification that insulates against regional economic shocks.

Forensic Wealth Audits: Celebrity Spouses

The “Padel Premium”: Revenue per Square Foot in 2026

The strategic significance of Bannatyne’s 2026 padel court rollout cannot be overstated. This is not trend-chasing; it is high-margin utilization of underperforming land assets. The group has already launched all-weather courts at Ingleby Barwick and is advancing planning permissions for 20 additional courts across the portfolio, with confirmed 2026 openings in Norwich, Livingston, Basingstoke, Chafford Hundred, Stratford-upon-Avon, Colchester, and Grove Park. Padel courts operate at 60–70% utilization rates, command £20–£40 per hour in court fees, and require minimal incremental capital expenditure when installed on existing car parks or surplus land. Critically, these courts are available to non-members, functioning as a low-friction customer acquisition funnel that converts casual players into full health club subscribers. For a business where real estate is the primary fixed cost, increasing Revenue per Square Foot through padel represents pure margin expansion—an operational insight that distinguishes Bannatyne from competitors still relying solely on membership dues.

The Debt-to-Equity Discipline: Avoiding the Leverage Trap

As Lead Data Researcher, the capital structure of Bannatyne Group warrants particular attention. Unlike competitors who pursued leveraged rollups during the low-interest-rate era of 2019–2021 and are now facing refinancing cliffs, Bannatyne has maintained a lean debt profile. The trauma of the 2008 Anglo Irish Bank collapse—where a £180 million facility became a deadweight liability—instilled a permanent aversion to over-leveraging. The 2026 accounts show a business that has absorbed £2 million in National Insurance increases and 11% energy cost exposure without resorting to distressed asset sales or dilutive equity raises. This capital-light philosophy enabled the December 2025 acquisition of Beechdown Leisure Club in Basingstoke and the January 2026 purchase of Clarice House hotel and spa without jeopardizing the core balance sheet. In an era where energy tariffs have become a material cost pressure for UK leisure operators — a headwind Bannatyne himself has publicly attributed to government policy, Bannatyne’s operational efficiency—closing underperforming clubs in Manchester while opening in high-demand zones—has proven more valuable than financial engineering.

Performance Audit: FY 2025/2026 Financial Indicators

| Data Point | Growth Trend | FY 2025/2026 |

|---|---|---|

| Total Revenue | +6% YoY | £158,000,000 |

| Operating Profit | +5.4% YoY | £27,200,000 |

| EBITDA | Stable | £43,700,000 |

| Member Count | Active Growth | 219,743 |

| Pre-Tax Profit | +9% YoY | £15,700,000 |

| Energy Cost Exposure | 11% of Cost Base | Managed |

| Key Diversifier | Padel Court Expansion | 20+ New Sites (2026) |

High-Yield Diversification: International Real Estate and the Luxury Wellness Hedge

Bannatyne’s non-gym assets function as critical inflation hedges and currency diversifiers within the broader portfolio. The group operates three premium hotels—the Charlton House Spa Hotel in Somerset, the Bannatyne Spa Hotel in Hastings, and a third property in the North East—alongside an integrated network of 45 luxury spas that are co-located with health clubs. This ecosystem generates ancillary revenue streams that are less cyclical than pure gym memberships; spa day passes and hotel stays capture discretionary spend from non-members while deepening retention among existing subscribers. The luxury spa market growth in the UK premium segment continues at 8–10% CAGR, and Bannatyne’s 45-spa network represents the largest integrated spa-health club operation in Britain.

The international HNW real estate component provides a further buffer against UK energy cost volatility and sterling weakness. Bannatyne maintains a villa in Portugal’s Algarve, purchased in 2016 and situated minutes from the beach, which functions as both a personal retreat and a euro-denominated asset. While his former French Riviera villa was liquidated post-divorce, the Portuguese holding remains, offering geographic diversification outside the UK tax and energy regime. The UK hotel portfolio, expanded through the 2015 Clarice House acquisition and the 2025 Beechdown purchase, provides hard-asset collateral that appreciates independently of the subscription revenue engine. For UHNW individuals analyzing Duncan Bannatyne property portfolio 2026, the key insight is that these assets are not passive holdings; they are operational extensions of the wellness brand that cross-sell memberships, spa treatments, and hospitality experiences.

Entertainment Wealth: From Music to Real Estate

The Operator’s Evolution: Media Legacy vs. Asset Reality

The final component of the 2026 Bannatyne audit is the reconceptualization of his public persona. Between 2005 and 2015, Bannatyne was defined by his Dragons’ Den “TV Investor” identity—deploying capital into 36 businesses, cultivating a Twitter following of 600,000+, and engaging in speculative side ventures including a £7,000 cameo in a Guy Ritchie film. That persona generated media capital but operational distraction. His 2015 exit from the show, alongside Kelly Hoppen and Piers Linney, coincided with a decisive strategic choice: by 2016, he had sold all his Dragons’ Den investments and redirected 100% of his focus to the Bannatyne Group.

This transition from “TV Investor” to “Hard-Asset Operator” is the single most important factor in the doubling of the Group’s enterprise value over the past decade. Where Peter Jones diversified horizontally into telecoms, retail, and logistics, and where Theo Paphitis spread capital across retail, property, and licensing, Bannatyne chose vertical depth. He invested in a sector-leading apprenticeship program, delegated to fitness-industry specialists rather than media personalities, and refined site-level KPIs. The result is a 3,000-employee operation where nearly all senior leadership has risen through internal progression. The 2026 financial results—delivered against employer National Insurance hikes, energy tariff chaos, and inflationary wage pressure—are proof that operational focus outperforms celebrity capital allocation. For UHNW individuals rebuilding after personal or legal setbacks, the Bannatyne blueprint is clear: strip away the speculative periphery, concentrate on cash-generating operational excellence, and allow EBITDA compounding to restore net worth over time.