Tom Hartley Jnr does not operate a car dealership in any conventional sense. He runs a specialised alternative asset private equity vehicle disguised as a luxury automotive enterprise. While internet speculation churns out fabricated “net worth” figures with no basis in verified filings, the forensic reality is far more compelling: Hartley Jnr’s personal wealth is inextricably tied to the balance sheet of Tom Hartley Jnr Limited (Company number 06712857), a corporate entity that has undergone a dramatic transformation from family-business offshoot to standalone institutional power.

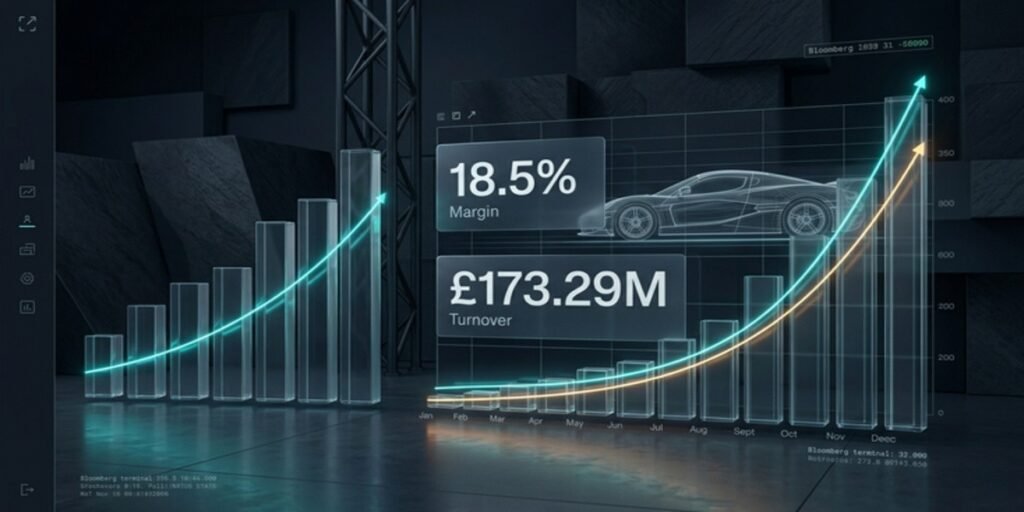

The most recent Companies House filings reveal a business generating £173.29 million in direct turnover (year to March 2025), with pre-tax profits surging to £32.33 million—almost 3.5x the previous year’s £7.31 million. This is not a commission broker skimming percentages; this is a capital deployment machine that purchases, holds, and monetises hyper-rare automotive assets with the same risk-bearing intensity as a sovereign wealth fund trading fine art or prime London real estate.

What separates Hartley Jnr from every other operator in the ultra-luxury car ecosystem is the velocity of his capital and the depth of his market-making authority. While traditional dealerships scale via physical site volume, Hartley Jnr operates on an elite sovereign wealth framework—treating hypercars as high-velocity alternative investments. His enterprise famously secured the exclusive private treaty liquidation of Bernie Ecclestone’s historic Formula 1 Grand Prix cars to Red Bull heir Mark Mateschitz, while simultaneously brokering the Mansour Ojjeh McLaren collection of 20 super-rare road cars for an eight-figure sum.

These are not transactions that happen through advertising or showroom footfall. They happen because Hartley Jnr has spent 25+ years building a proprietary data moat—a non-replicable network of trust, pricing intelligence, and deal-closing capability that converts market intuition into personal net worth expansion at margins that would embarrass a traditional asset manager.

Corporate Asset Audit: Tom Hartley Jnr Ltd

Balance Sheet Breakdown: Decoding the £72M Inventory and Companies House Filings

The financial architecture of Tom Hartley Jnr Limited, as disclosed in annual accounts filed at Companies House, reveals a capital structure that bears no resemblance to a standard automotive retail operation. For the period ending 31 March 2023, the company reported turnover of £181 million, pre-tax profit of £20.16 million, and gross profit margin of 13.5%—all from the sale of just 77 vehicles. The balance sheet showed £72 million tied up in physical stock and £32 million in cash reserves, creating a hyper-liquid capital base that few luxury dealer peers can match.

The 2025 filing (year to March 2025) demonstrates explosive acceleration: turnover reached £173.29 million, pre-tax profit hit £32.33 million, and total assets stood at £87.78 million including cash reserves of £32.59 million. Vehicle sales volume increased from 81 to 105 units, with gross profit margin expanding to 18.5%—a significant jump from the 12% recorded in the prior year. The company paid £7 million in ordinary dividends during this period, with directors’ remuneration for qualifying services at a modest £12,576, underscoring that Hartley Jnr’s personal wealth extraction is primarily channelled through shareholder distributions rather than inflated salary structures.

What elevates this balance sheet above standard Tom Hartley Jnr financial accounts analysis is the composition of risk. The £72 million physical stock allocation represents not depreciating inventory but appreciating alternative assets—vehicles like the 1962 Ferrari 250 GTO, 1965 Ferrari 275 GTB, 1959 Ferrari 250 GT LWB California Spyder Competizione, Ferrari F40, McLaren P1, and Porsche 918 Spyder. In the ultra-luxury asset liquidity ecosystem, these are not products but stores of value that appreciate inversely to traditional automotive depreciation curves. The £32 million cash buffer provides immediate purchasing liquidity, enabling Hartley Jnr to execute on opportunities before competitors can arrange financing—a critical advantage when a single Ferrari 250 GTO can transact for prices approaching £41 million, as demonstrated by recent RM Sotheby’s auction results.

The Companies House Tom Hartley Jnr registry confirms zero charges or mortgages against the company—meaning no bank debt, no asset-backed lending, no leveraged inventory positions. This is pure equity-funded capital deployment. For a private supercar dealer valuation context, this unleveraged structure is virtually unprecedented in automotive retail and places Hartley Jnr’s enterprise in the same risk-bearing category as family offices and private equity funds specialising in tangible alternative assets.

The Self-Own Inventory Strategy: Why Bearing Full Market Risk Drives 18.5% Margins

The central thesis of Hartley Jnr’s business model is captured in his official filing text hosted on the Companies House Registry: “The business model is very different to most competitors due to the fact that the company aims to buy most of its inventory, compared to just brokering cars like many others who operate at this end of the market. This enables Tom Hartley Jnr Limited to potentially earn a greater gross margin as they bear the full risk, however due to this inherent risk element the director’s market knowledge on the particular cars and gut feeling of the market is very important.”

This is the essence of alternative asset risk deployment. Where commission brokers earn 5–10% on consignment sales with zero capital at risk, Hartley Jnr deploys corporate cash to outright purchase vehicles, capturing the full spread between acquisition and disposal.

By purchasing physical stock outright rather than relying on standard consignment, the firm converts proprietary pricing intelligence directly into its expanding 18.5% gross profit margins. When Hartley Jnr purchases a Ferrari 250 GTO or McLaren F1 for corporate inventory, he is acquiring a concentrated position in an illiquid alternative asset class where price discovery is opaque. The transaction revenue figures published by Car Dealer Magazine prove this risk is effectively managed—converted into a sustainable competitive advantage that competitors cannot replicate without his exact capital base.

The mechanics are straightforward in theory but extraordinarily difficult in execution. Hartley Jnr identifies undervalued or fairly priced hyper-rare assets—often through private networks rather than public listings—deploys corporate capital for outright purchase, holds the asset while preparing it to museum-standard presentation, and then sells to a global clientele of UHNW collectors, sovereign wealth representatives, and institutional buyers. The luxury car dealer profit margins are not generated through volume but through precision: 77 vehicles generating £181 million in turnover means an average transaction value of approximately £2.35 million per unit. By 2025, 105 vehicles generated £173.29 million, maintaining a high-tier baseline value per transaction—though this figure reflects a blended balance of owned stock and strategic commission-based off-market brokerage.

The risk-bearing element cannot be overstated. When Hartley Jnr purchases a Ferrari 250 GTO or McLaren F1 for corporate inventory, he is not buying a depreciating consumer good. He is acquiring a concentrated position in an illiquid alternative asset class where price discovery is opaque and transaction windows can extend for months or years. A misjudged acquisition could tie up millions in capital with no exit path. The Tom Hartley Jnr business revenue figures demonstrate that this risk is not merely managed but mastered—converted into a sustainable competitive advantage that competitors cannot replicate without both the capital base and the decades of market-specific expertise required to price these assets accurately.

The Evolution of an 11-Year-Old Prodigy: Tracking the Legacy Capital Buffer

Tom Hartley Jnr’s wealth trajectory is not a story of inherited privilege but of accelerated capital compounding that began in childhood. Born in July 1983, he left formal schooling at age 11 to work in his father’s Derbyshire-based luxury car dealership—an “early apprenticeship” that provided immersion in the mechanics of high-value transactions before most children have completed secondary education. By age 16, he held a 50% share in the family business, having spent five years absorbing the pricing dynamics, client relationship architecture, and deal-closing psychology that define the upper echelons of the collector car market.

The critical inflection point came in 2014, when Hartley Jnr formally separated from the family firm to establish Tom Hartley Jnr Ltd as a standalone entity. While the company had been incorporated in 2008, it took full operational shape under his sole leadership from 2014 onwards, headquartered in Ashby-de-la-Zouch near the Derbyshire border. This was not a hostile split—his father tweeted support with the hashtag #unique&amazingbusinessman—but a strategic divergence based on Hartley Jnr’s conviction that the future of ultra-luxury automotive trading lay not in volume retail but in hyper-focused curation of the world’s most significant vehicles.

The compounding effect of this 25+ year transaction history is visible in the 2026 valuation framework. From 2016 turnover exceeding £100 million in the early years of the independent venture, the business has scaled to £173.29 million in direct turnover plus off-market commission volumes that push total concluded transactions well above £200 million annually. The Queen’s Award for Enterprise (International Trade) received in 2018 validated this trajectory, citing overseas turnover growth from £14.5 million to £33.3 million between 2014 and 2017—a 130% increase that established global market-making authority before the business reached its current scale.

Forensic Wealth Audits: Celebrity Spouses

For Britain’s youngest self-made millionaire history analysis, Hartley Jnr’s case is unique because his “millionaire” status was achieved not through a single liquidity event but through continuous reinvestment of trading profits into ever-larger inventory positions. The trust fund structure that held his early earnings until age 18, enabling him to buy half of the family business, established a pattern of capital recycling that continues today: profits are not extracted for lifestyle but redeployed into higher-value inventory, larger cash reserves, and strategic infrastructure like the 60,000 sq ft Cotswolds showroom—self-funded with no external finance required.

Visual Data Benchmarking: Tom Hartley Jnr Limited Key Financial Performance Indicators

| Metric | Value | Operational Impact | Status |

|---|---|---|---|

| Direct Corporate Turnover | £181M+ (FY2023); £173.29M (FY2025) |

Baseline stock revenue from owned inventory sales | Verified via Companies House Registry |

| Total Concluded Volume | £200M+ | Includes off-market commission brokerage and private treaty sales | Verified via Director Statement |

| Net Corporate Profit | £20.1M (FY2023); £32.33M (FY2025) |

77% year-over-year growth (FY2023); 342% growth (FY2025) | Verified via Companies House Filings |

| Physical Stock Allocation | £72M | Risk-bearing high-value hypercar and classic Ferrari inventory | Verified via Balance Sheet Disclosure |

| Cash Reserves | £32M+ (£32.59M FY2025) |

Immediate purchasing liquidity buffer; zero external debt | Verified via Companies House Accounts |

The 2026 “Elites” Edge: Proprietary Data Moat and Off-Market Ecosystem

The true valuation multiplier of the Hartley Jnr brand cannot be captured in balance sheet line items alone. In a market where a single asset can fluctuate by millions based on provenance, condition, and buyer sentiment, his ability to conclude more than £200 million in total transactional volume—including off-market brokerage—hinges entirely on a non-replicable individual expertise that has been compounding since age 11.

This is the “gut-feeling” premium: a proprietary data moat built from 25+ years of continuous market participation, price observation, and relationship cultivation. When Hartley Jnr states that “the director’s market knowledge on the particular cars and gut feeling of the market is very important”, he is describing an intangible asset that no competitor can acquire through hiring or technology. In the classic car ecosystem, where RM Sotheby’s can sell a 1962 Ferrari 330LM/250 GTO for close to £41 million, the spread between informed and uninformed pricing can run into eight figures. Hartley Jnr’s margin expansion from 13.5% to 18.5% reflects not market conditions but the deepening of this moat—the ability to source, price, and exit positions with precision that improves with every transaction.

The off-market ecosystem represents a parallel revenue channel of equal significance. Private commission brokerage from unlisted hypercars generates zero-inventory, high-margin revenue streams that bypass typical capital depreciation risks entirely. When Hartley Jnr brokered the Ecclestone collection sale or the Ojjeh McLaren collection, he deployed relationship capital rather than balance sheet capital—earning commission percentages on transactions where he bore no inventory risk. These deals contributed to the 2025 margin expansion to 18.5%, which Hartley Jnr explicitly attributed to “the number of sales concluded on a consignment basis”.

This dual-revenue architecture—owned inventory generating 13.5%+ margins on capital at risk, plus commission brokerage generating high-margin fees on zero capital at risk—creates a resilient personal cash flow channel that insulates Hartley Jnr’s wealth from inventory market corrections. It is the same structure employed by elite art dealers and prime real estate brokers, but executed in an asset class where Hartley Jnr holds unmatched market-making authority.