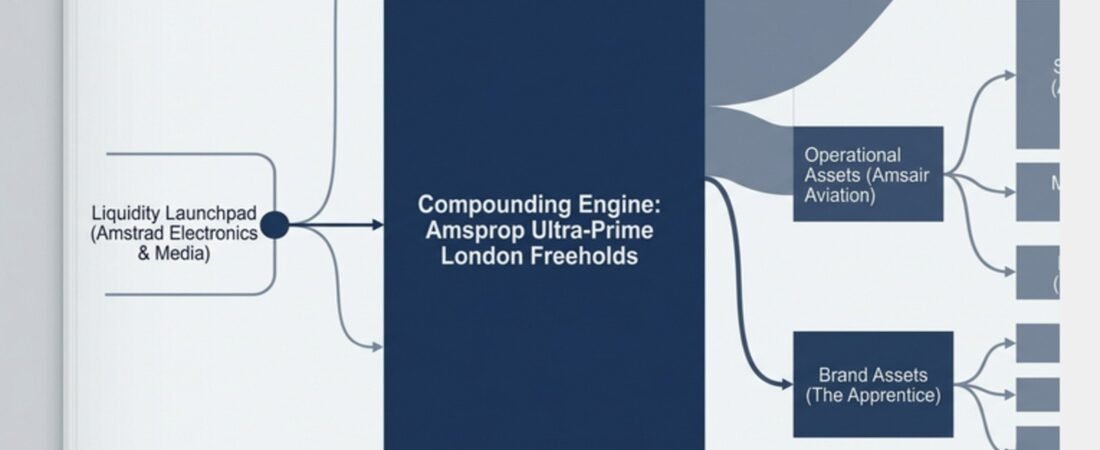

The mainstream narrative surrounding Lord Alan Sugar remains stubbornly anchored to consumer electronics folklore and reality television theatrics. Decades of BBC programming have cemented a public perception that his billionaire status is the residual fruit of Amstrad personal computers, the e-m@iler, or the commercial momentum of The Apprentice. This is a category error. Sugar’s 1968 founding of Amstrad was never the terminus of his wealth architecture; it was the liquidity launchpad. The durable, compounding engine of his fortune is a defensive, low-leverage commercial real estate operation concentrated in ultra-prime Central London and core City of London freeholds—a strategy that has insulated his capital from the volatility plaguing consumer tech and media markets.

According to the Sunday Times Rich List historical baselines, Lord Sugar’s net worth holds steady at an estimated £1.1 billion, placing him comfortably among Britain’s top billionaires.

The 2026 Sunday Times Rich List — published 15 May 2026 — documented 157 UK billionaires, down from a peak of 177 in 2022, as an exodus of wealthy individuals left the UK following Labour’s non-dom tax reforms. Sugar’s retention of billionaire status through this period is itself a forensic signal of his portfolio’s defensive construction.

Yet the critical forensic signal is not this headline figure, but the newly filed corporate data for his umbrella holding vehicle, Amshold Group Limited (Company number 08557403) (Companies House Filing, Dec 2025).

For the financial year ending 30 June 2025, Amshold reported a surge to £14.1 million in pre-tax profits—a tripling from the £932,000 recorded in the prior period—achieved not through speculative scaling, but through aggressive debt reduction, tactical property liquidations, and the deliberate minimization of leverage in a hostile, high-interest UK economy. The following matrix isolates the true hierarchy of his wealth engine.

Amshold Group Asset Balance Sheet Matrix (2026)

| Holding Entity / Asset | Primary Focus | Corporate Signal / 2026 Status | Wealth Status |

|---|---|---|---|

| Amshold Group Ltd | Parent Umbrella / Investment | Reported £14.1M pre-tax profit in latest filings; external corporate liabilities cut from £85.7M to £75M. | Primary wealth engine |

| Amsprop Estates | Ultra-prime Central & City of London freeholds | Yield and capital appreciation via active asset redevelopment (e.g., core Minories holdings). | Primary asset base |

| Amsair Executive Aviation | Executive jet charter & private operations | Operates Cessna fleet & Embraer Legacy 650 (G-SUGA). Managed by Air Charter Scotland from London Luton. | High-overhead operational asset |

| Amscreen Limited | M2M & retail digital signage technology | Led by CEO Simon Sugar; face-detection (OptimEyes) integration; portfolio exit completed via sale to Bauer Media Group. | Mid-tier tech liquidation |

| The Apprentice (BBC) | Media & public relations platform | Bespoke and standard seed funding (£250k per winner) deployed through balance-sheet capital via corporate joint ventures (e.g., Amsvest). | Brand asset / Incidental revenue |

The Amshold Pivot: How Commercial Real Estate Eclipsed the Amstrad Legacy

Amstrad, conceptualized from his family’s roots in a Hackney council estate but launched formally via Central London commercial channels, generated genuine industrial scale in consumer electronics. Yet the company’s zenith valuation in the mid-to-late 1980s proved ephemeral. In 2007, Sugar disposed of his remaining interest in Amstrad to BSkyB for a transaction valued between £125 million and £135 million—a finite, terminal sum. That same year, he sold his remaining minority stake in Tottenham Hotspur FC to ENIC for £25 million. While Sugar had already stepped down as Spurs chairman in 2001, this 2007 transaction finalized a 16-year financial association with the football club. Sugar later donated £3 million from the proceeds to the refurbishment of the Hackney Empire theatre — a rare public gesture connecting his corporate liquidity events to his East End origins.

Impressive, but insufficient to sustain billionaire status across two decades of inflation and market cycles.

The compounding valuation occurred elsewhere. In 1985, Sugar established Amsprop, a privately owned real estate vehicle now controlled for over 20 years by his son, Daniel Sugar. Amsprop’s mandate is surgical: acquisition of ultra-prime Central London and core City of London freeholds, active refurbishment, and long-term yield extraction. The portfolio has focused on institutional-grade London assets, such as prime commercial sites across the Minories and historical Bishopsgate freeholds.

As 2014 Apprentice winner Mark Wright later relayed, Sugar’s own doctrine is blunt: “You make money from property and do business for fun.”

While tech entrepreneurs like Sir James Dyson face massive capital expenditure volatility to maintain market share, Alan Sugar’s modern wealth architecture mimics that of traditional estate dynasties—relying on high-barrier freehold assets in prime London zones to insulate capital from market downturns. The electronics empire provided the initial war chest; the property empire provided the perpetual annuity.

You May also Read–

- Who is Louise Bonsall? Michael Owen’s Wife & the Force Behind the Owen Dynasty

- Cassie randolph net worth

- Ifet Anwar: Leading Scottish Property Solicitor and Advocate

- Bill Gaither net worth

The 2026 Debt-Reduction Playbook: Inside Amshold’s £14.1M Profit Surge

A forensic analysis of Amshold Group’s latest UK Companies House filings, published in December 2025 for the year ending 30 June 2025, reveals a textbook defensive maneuver from a high-net-worth operator navigating a hostile credit environment. Pre-tax profit rocketed to £14.1 million, up from £932,000 in the prior year and a staggering reversal from the £29.1 million pre-tax loss recorded two years earlier. Turnover held relatively flat at £8.9 million (versus £8.7 million), confirming that the profit surge was not driven by operational expansion but by balance-sheet restructuring.

The primary catalyst was the liquidation of selected non-core assets rather than the accretion of new leverage. On 1 October 2024, Amshold sold The Crosspoint at 117-121 Bishopsgate for £24 million. This disposal, combined with a second investment property sale, generated a combined profit of £9.9 million. Critically, the group used these proceeds to slash debt exposure: debt due to associated companies fell from £85.7 million to £75 million. Amshold’s operating profit rose modestly from £3.1 million to £3.6 million, but the real balance-sheet repair lay in the net revaluation gain of £800,000—recovering from a £1.2 million deficit in the prior period—pushing net assets from £13.4 million to £23.8 million.

The filings explicitly acknowledge the macro headwinds: “The market for quality London freehold investment property is difficult with high interest rates, uncertainty and fluctuating valuations.” Sugar’s response was not to chase yield through expensive floating-rate financing—the standard trap for overleveraged REITs and private equity landlords—but to fortify. Amshold noted it holds fixed long-term funding, leaving it “extremely well placed” to acquire distressed prime assets from weaker hands. For high-net-worth principals operating in the 2026 London commercial real estate market, the Sugar playbook offers a stark contrast to growth-at-all-costs strategies: when debt is expensive, reduce it; when valuations are uncertain, crystallize gains on non-core stock; when competitors are overleveraged, sit on dry powder.

Secondary Holdings: From Amsair Aviation to The Apprentice Fee Realities

A rigorous wealth audit demands that peripheral ventures be weighed against the core property engine and found wanting. Amsair Executive Aviation, founded in 1993 and operated by Daniel Sugar, runs a charter fleet including multiple Cessna aircraft and the flagship Embraer Legacy 650, registration G-SUGA—a $30 million business jet managed by Air Charter Scotland from London Luton. The asset is operational, not financial: it consumes maintenance, crew, and hangar capital, and its charter revenue is incidental to a billion-pound balance sheet.

Amscreen Limited, the digital signage and machine-to-machine (M2M) technology arm managed by Simon Sugar, integrated face-detection analytics (OptimEyes) into retail and medical screens. In September 2025, Bauer Media Group acquired Amscreen, removing it from the Amshold stable. The exit validates its mid-tier status: material enough to attract a national media buyer, but never a primary wealth driver. At the time of acquisition, Amscreen employed more than 60 people and operated a 60,000 sq ft headquarters in Bolton, Lancashire — Europe’s largest manufacturer of digital outdoor signage by installed estate.

Then there is The Apprentice. Sugar’s BBC talent fee is estimated between £500,000 and £1.5 million annually—a sum that is entirely incidental to a billionaire entity. The program’s financial significance lies not in his salary but in the Amsvest joint-venture structure, through which Sugar injects approximately £250,000 in seed capital per winner (taking a 50% equity stake via holding vehicles). This is brand architecture, not income dependency.

The Tropic Skincare Anomaly: Demonstrating the distinction between the standard winner’s pot and exceptional talent, Sugar carved out a bespoke investment path for 2011 runner-up Susie Ma, injecting an initial £200,000. When Ma bought out his 50% stake, Sugar did not just secure a vague return; he extracted a documented £11 million dividend payout before fully exiting. By 2024, Tropic had grown to £68 million in annual revenues with £8.7 million in pre-tax profits — making Sugar’s original £200,000 outlay one of the highest-returning venture bets in Apprentice history on a return-multiple basis.

Also read–

- Dragons’ Den Net Worth 2026: Forensic Ranking of the UK’s Richest Investors

- How Founders Build Personal Brand UK 2026

- UK Richest TV Presenters 2026 Ranked

Structural Architecture: Peerage Tax Traps and Intergenerational Control

The “Lords” Tax Trap

No audit of Sugar’s 2026 position is complete without examining the failed attempt to shield his wealth from a £186 million tax bill. In the 2021-2022 tax year, Amshold Group paid Sugar a £390 million dividend—the accumulation of years of property sales and deal proceeds. Sugar attempted to declare himself a non-UK resident for tax purposes, a standard high-net-worth expatriation strategy that would have nullified UK liability on the dividend.

The attempt collapsed because of a specific statutory trap. Under Section 41 of the Constitutional Reform and Governance Act 2010, serving members of the House of Commons or House of Lords are automatically treated as resident and domiciled in the United Kingdom for income tax, capital gains tax, and inheritance tax purposes—irrespective of physical presence. Sugar, elevated to the Lords in 2009 as a Labour peer and sitting as a crossbencher since 2017, was legally barred from the non-resident designation.

He had taken an initial formal leave of absence in 2022 and a subsequent leave in October 2025 — steps widely interpreted in the context of the preceding tax reporting, though he has not publicly confirmed this interpretation. Neither procedural step overrides the statutory residency deeming. After the Bureau of Investigative Journalism and The Sunday Times exposed the maneuver, Sugar paid the £186 million liability in full and is reportedly pursuing legal action against his tax advisers for the oversight. The episode serves as a stark warning to peerage-tier HNWs: a seat in the Lords confers political status, but it permanently forecloses standard offshore tax expatriation strategies.

Intergenerational Control Architecture

Recent Companies House filings from early 2026 reveal a deliberate recalibration of Sugar’s corporate control structure. On 31 March 2026, Amsprop Property Company Limited filed a PSC07 notice: the cessation of The Lord Sugar Family Trust as a Person of Significant Control, effective 25 March 2026. Simultaneously, a PSC01 notification re-registered Alan Michael Sugar as the direct individual PSC. A further PSC04 change of details was filed on 23 April 2026. These are not cosmetic filings; they signal a consolidation of direct personal control over the property holding vehicle, even as day-to-day operations transition to the next generation.

The intergenerational architecture is already embedded. Daniel Sugar (appointed director of Amshold International Limited on 17 December 2000) directs Amsprop and Amsair. Simon Sugar (appointed director of Amshold International on 8 January 2004) previously helmed Amscreen. Both brothers, alongside sister Louise Sugar (appointed 15 May 2000), occupy board seats across the Amshold network. Yet the PSC notifications confirm that absolute structural control—via direct shareholding and trust mechanisms—remains with Lord Sugar. The sons execute acquisitions, manage tenant relationships, and oversee refurbishment programs, but the freehold titles and strategic debt decisions remain centrally commanded. This is dynastic wealth preservation in its corporate form: operational delegation paired with structural absolutism.

Frequently Asked Questions

Q: What is Lord Alan Sugar’s exact net worth?

The Sunday Times Rich List historically benchmarks his fortune at an estimated £1.1 billion. This valuation is strictly property-anchored and insulated from public tech-equity volatility, placing him consistently among the top tier of Britain’s wealthiest individuals.

Q: Does Alan Sugar still own Amstrad or Viglen?

No. Amstrad was sold to BSkyB in 2007 in a transaction valued up to £135 million. His education and public sector IT provider, Viglen, was fully sold to XMA in 2014. Neither legacy enterprise remains in his portfolio; both served as critical liquid entry points to fund his multi-decade commercial real estate pipeline.

Q: How much of his personal capital does Lord Sugar invest in Apprentice winners?

Sugar does not write personal cheques. Standard winners receive a £250,000 investment deployed directly from his corporate balance sheet via Amsvest Limited, with his holding structure capturing a 50% equity stake. The commercial reality of these deals is best highlighted by the Tropic Skincare anomaly: Sugar carved out a bespoke, non-winner investment path for 2011 runner-up Susie Ma. Before Ma bought out his remaining 50% shares to regain full ownership, Sugar extracted a documented £11 million cash dividend from the vehicle, demonstrating that The Apprentice serves as a rigorous private-equity funnel.

Q: Why did Lord Sugar’s non-residency tax strategy fail?

Following a massive £390 million dividend payout from Amshold, Sugar attempted to declare himself a non-UK resident to mitigate a £186 million tax liability. The maneuver failed because of Section 41 of the Constitutional Reform and Governance Act 2010. Under UK law, sitting members of the House of Lords are permanently and automatically deemed UK-domiciled and resident for tax purposes. Because he entered the Lords as a peer in 2009, even a formal leave of absence could not override the statutory tax designation, forcing him to repay the liability in full.

Q: Who will inherit and control the Sugar property empire?

The architecture is structured entirely around intergenerational corporate continuity. While Lord Sugar consolidated absolute, direct control over the real estate engine via individual Person of Significant Control (PSC) updates at Companies House, his children are deeply embedded. Daniel Sugar commands day-to-day operations as director of the core real estate arm (Amsprop) and aviation fleet (Amsair), while Simon Sugar and Louise Sugar maintain executive oversight across the parent umbrella network.

Disclaimer & Editorial Notes

This profile functions strictly as an independent forensic corporate case study and public asset audit. All corporate valuations, property holdings, and net worth indexing are compiled exclusively from high-authority public records, Companies House filings, and historical media indices. Elites Mindset operates with absolute editorial independence and maintains no corporate affiliation, endorsement, or commercial relationship with Lord Alan Sugar, Amsprop, or the BBC’s The Apprentice. The insights provided herein are for educational, corporate strategy, and analytical purposes only and do not constitute financial, legal, or investment advice.

Suggested reads–

- Sarra Kemp: Everything About Chris Hoy’s Wife and Her Remarkable Story

- Matteo Mantegazza: The Son of Award-Winning Actress Greta Scacchi

- Alice Bamford: Film Producer, Global Environmental Educator, and Scion of Britain’s Billionaire Bamford Dynasty

- Norraco transact app