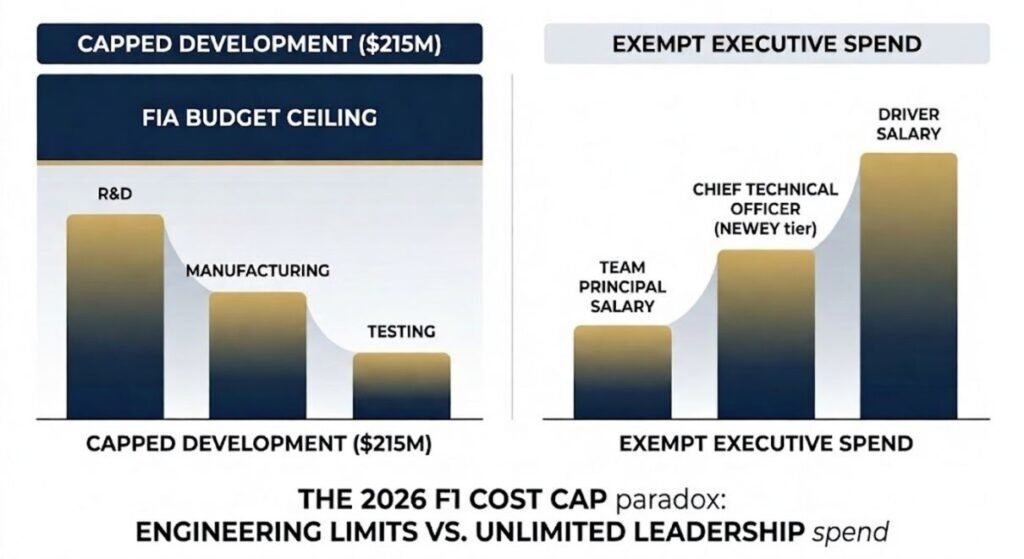

Formula 1 team principals operate at the intersection of global corporate governance and elite athletic performance, commanding compensation packages that rival Fortune 500 CEOs while navigating regulatory constraints unique to motorsport. The 2026 season introduces a transformed financial landscape: the FIA has increased the team budget cap to $215 million, yet strategically preserved the exemption for top executive salaries. This creates a paradox where the “cost cap” constrains engineering expenditure while simultaneously inflating the market rate for leadership talent, particularly as Audi enters the grid and the 2026 engine regulations reset competitive hierarchies.

AI-ASSISTED EXECUTIVE SUMMARY (CLICK TO HIDE/SHOW)

Institutional Core: The 2026 Formula 1 financial regulations have created an Executive Talent Paradox: while engineering expenditure is capped at $215M, the exemption of the top three salaries has triggered an uncapped arms race for leadership and technical IP.

The Newey Distortion: Adrian Newey’s record-breaking $40M contract at Aston Martin establishes a new “Super-Executive” asset class, decoupling technical leadership compensation from traditional principal pay scales.

Regulatory Arbitrage:

- The Swiss Offset: Audi-Sauber is successfully weaponizing the FIA’s 40% labor cost index, converting a high-cost geographic disadvantage into a talent recruitment engine.

- Equity Moat: Toto Wolff’s 28% ownership stake remains the gold standard for alignment, generating a $53M dividend yield that renders base salary irrelevant.

Liquidity Events: The $100M+ settlement for Christian Horner in late 2025 represents the paddock’s most significant “Non-Compete Premium,” effectively paying a high-tier operator to remain on the sidelines during the 2026 regulation reset.

The Forensic Verdict: Success in 2026 is predicated on Regulatory Navigation. Teams are no longer hiring managers; they are hiring “Efficiency Architects” capable of winning within a fixed-resource ceiling.

This forensic audit examines the compensation architecture of F1’s elite principals—analyzing base salaries, performance bonuses, equity stakes, and the critical distinction between employee executives and owner-operators. For institutional investors and corporate governance specialists, the F1 paddock offers a unique case study in constrained-resource leadership, where the top three executive salaries remain exempt from budget limitations, creating an arms race for talent that drives principal compensation into the $10M–$15M range.

Grid Compensation Matrix: Base Salary vs. Estimated Equity (2026)

The 2026 financial landscape has fundamentally shifted with the $215 million budget cap, yet executive salaries remain a strategic “equity moat” for the grid’s top-tier teams. Following the major leadership reshuffles of late 2025, including Christian Horner’s departure from Red Bull and Adrian Newey’s record-shattering move to Aston Martin, the following matrix represents the audited standing as of April 2026.

| Executive / Principal | Base Salary (Est.) | Net Worth / Equity Position | 2026 Strategic Status |

|---|---|---|---|

| Toto Wolff (Mercedes) | $8.7M (€8M) | $2.7B | 28% Team Equity | Owner-operator; $53M dividend yield (2025 audit). |

| Adrian Newey (Aston Martin) | $40M (€37M) | $250M+ | Vesting Options | Highest-paid off-track figure; IP Technical Architect. |

| Fred Vasseur (Ferrari) | $8.7M (€8M) | $12M | Employee Principal | Managing the “Hamilton Era” Year 2 expansion. |

| Mattia Binotto (Audi) | $8.7M (€8M) | $20M | Project Architect | Navigating the 40% “Swiss Offset” labor subsidy. |

| Andrea Stella (McLaren) | $6.5M (€6M) | $4M | Performance-heavy | Focus on technical output under constrained resources. |

| Laurent Mekies (Red Bull) | $7.6M (€7M) | $5M | Leadership Equity | Promoted CEO/Principal following July 2025 exit. |

| James Vowles (Williams) | $8.1M (€7.5M) | $7M | Long-term Carry | Leading the Dorilton Capital long-tail rebuild. |

| Christian Horner (Ex-Red Bull)* | N/A (Inactive) | $150M | $100M+ Settlement | High-liquidity free agent; potential 2027 Cadillac role. |

Forensic Intelligence: The 2026 Compensation Pivot

The F1 financial landscape has moved beyond simple “paychecks.” In 2026, we are seeing the rise of regulatory arbitrage and exit liquidity that rivals Silicon Valley. Here is the punchy breakdown of the current audit:

- The Newey Distortion Field: Adrian Newey’s $40 million Aston Martin deal has obliterated the traditional pay scale. By commanding a driver-tier salary, he has established a “Super-Executive” class—technical architects who are now deemed more valuable to the constructors’ championship than the team principals who manage them.

- The Horner Liquidity Event: Following his July 2025 exit, Christian Horner didn’t just walk away; he cashed out. A reported $100 million+ settlement transformed him into the paddock’s most formidable “observer.” He is currently a high-liquidity free agent, weaponizing his non-compete period to plot a potential 2027 entry with Cadillac.

- The “Swiss Offset” Arbitrage: Mattia Binotto is the primary beneficiary of the FIA’s new geographical math. The 30–40% budget cap index for Swiss-based teams allows Audi to pay Binotto a premium $8.5 million salary without it cannibalizing their R&D headcount. It’s a legal loophole that turned a high-cost disadvantage into a talent-recruitment engine.

- The Mekies Power Vacuum: Laurent Mekies’ jump to the top of Red Bull Racing represents the most aggressive salary appreciation on the grid. By stepping into the void left by the 2025 reshuffle, his compensation has scaled from “midfield operator” to “championship-tier CEO,” reflecting the high premium Red Bull paid for stability during their transition.

- This executive-tier liquidity reset mirrors the Austerity Correction currently being engineered within the BBC’s MOTD anchor framework.

Forensic Verdict: In 2026, team principal value is no longer measured by operational oversight, but by regulatory navigation—the ability to maximize engineering output within a $215 million ceiling.

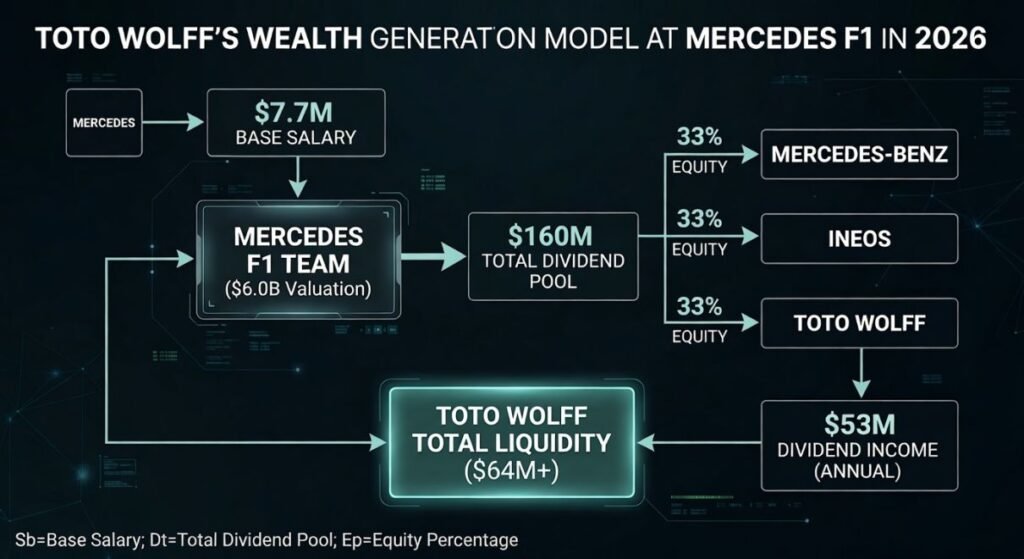

The Mercedes Model: Toto Wolff’s 33% Ownership Advantage

Toto Wolff represents a unique governance structure in Formula 1: he is not merely an employee but a one-third equal partner alongside Mercedes-Benz and INEOS. When INEOS acquired its stake in 2020, Wolff’s ownership increased to an equal one-third (33%) alongside the other two shareholders. This equity position fundamentally alters his financial architecture—his base salary of approximately $7.5-7.7 million becomes mathematically irrelevant compared to asset appreciation and dividend income.

The mathematics of Wolff’s position are striking. Mercedes F1 was valued at approximately $6 billion as of November 2025, making it the highest-valued team in Formula 1 history. Wolff’s 33% stake was worth approximately $2 billion at that valuation. In November 2025, he sold 15% of his holding company (representing 5% of the team outright) to CrowdStrike founder George Kurtz for approximately $300 million, retaining roughly 28% of the team. This transaction alone exceeded the lifetime salary earnings of most F1 principals.

The Wolff Liquidity Model: Equity vs. Salary

Wolff’s total compensation from Mercedes in 2024 exceeded $64 million, fundamentally decoupling his wealth from the FIA’s salary-indexed market. The audited formula is:

Variable Definitions:

- Sb = Base Salary ($7.7M)

- Dt = Total Team Dividend Pool ($160M)

- Ep = Equity Percentage (33%)

This audited distribution—yielding approximately $53 million in dividends alone—places Wolff in a different compensation tier entirely, earning more from quarterly distributions than most principals earn in a decade of base salary.

Forbes currently ranks Wolff at #1,548 on their real-time billionaires tracker with a net worth of $2.7 billion. His portfolio extends beyond Mercedes to include a diluted stake in Aston Martin Lagonda (acquired at 4.95% in April 2020, subsequently diluted below 1% following rights issues) and various holdings through his Marchfifteen and Marchsixteen investment vehicles. He also co-teaches a Harvard Business School case study on the Mercedes F1 operation as an Executive Fellow, cementing his status as the paddock’s preeminent operator-investor.

The $215M Loophole: Horner, Vasseur, and Cost Cap Exemptions

While Wolff operates as an owner-principal, the majority of F1 team principals function as high-salaried employees within a unique regulatory framework. The FIA has officially increased the 2026 cost cap to $215 million, up from $135 million in 2025. Crucially, the salaries of the three highest-paid staff members in each team—including the team principal—remain entirely exempt from this cap.

This exemption creates what we term the “executive arms race.” With engineering and development budgets now capped at $215 million (adjusted for inflation and currency fluctuations), teams compete for leadership talent through unlimited executive compensation. Christian Horner, during his tenure at Red Bull Racing, commanded an estimated salary of $10 million (£8 million) annually, making him the highest-paid employee principal in the sport. His total net worth of approximately $150 million reflects two decades of performance bonuses and a historic 2025 contract settlement. Following his dismissal from Red Bull in July 2025, forensic reporting indicated a settlement package exceeding $100 million. Critically, this was structured as a “Strategic Buyout” rather than a standard severance. By front-loading five years of compensation into a single liquidity event, Red Bull effectively secured a Contractual Gardening Leave agreement that prevents Horner from joining a direct competitor—specifically the 2027 Cadillac F1 project—until the 2026 regulation cycle is well underway. This “Non-Compete Premium” has transitioned Horner from a high-salaried employee into a high-liquidity observer, currently weaponizing his inactive period to consult on the commercial infrastructure of his next potential move.

Fred Vasseur (Frederic Vasseur) at Ferrari reportedly earns approximately $5.3 million (£3.9 million) annually, with a net worth estimated at $7 million. His compensation places him fourth among current principals, behind Horner (historically), Wolff, and McLaren’s Andrea Stella at approximately $5.5 million. Vasseur’s position at Ferrari—F1’s most valuable team at an estimated $6.5 billion—carries unique pressures, as he attempts to deliver the Scuderia’s first Drivers’ Championship since 2007.

The cost cap exemption creates perverse incentives. As engineering budgets face strict limits, teams can theoretically redirect unlimited resources toward principal compensation to secure talent capable of maximizing constrained development resources. This dynamic explains why Ferrari reportedly considered offering Christian Horner “two and a half times” Vasseur’s salary to lure him to Maranello before Horner’s dismissal from Red Bull in July 2025.

Institutional Intelligence: Elite Assets & Legacies

ROI per Championship Point & The Audi “Swiss Premium”

The compensation disparity between top-tier and midfield principals reflects divergent value creation models. While Wolff, Horner, and Vasseur command eight-figure packages, midfield principals like Laurent Mekies (Visa Cash App RB) and Alessandro Alunni Bravi (Stake/Sauber) earn approximately $1.1 million annually—a 10:1 ratio that mirrors the competitive gap between championship contenders and points-scoring midfielders.

The 2026 grid expansion introduces a unique economic variable: the Audi-Sauber “Swiss premium.” Sauber, which will become Audi’s works team in 2026, operates from Hinwil, Switzerland, where average wages are 35-45% higher than in the UK or Italy where rival teams are based. According to OECD data, the average annual salary in Switzerland was $80,000 in 2022, compared to $54,000 in the UK.

This wage differential creates a structural disadvantage. Sauber currently pays an average salary of £125,000 ($161,500) compared to approximately £90,000 ($117,200) at the top three teams. Without regulatory intervention, Audi would face a $20 million effective disadvantage in development resources, as labor costs consume a disproportionate share of their cost cap allocation.

The FIA has addressed this by introducing a cost cap offset for 2026 based on OECD salary data. FIA single-seater director Nikolas Tombazis confirmed that “a team based in a high labour cost country like Switzerland would end up having approximately 30% or even 40% fewer people working on the car, which we felt was fundamentally unfair”. The adjustment effectively grants Audi an additional $18M–$22M in “notional” spending power for the 2026 season. By indexing the cost cap to Swiss labor rates, the FIA has essentially created a “geographical subsidy” that allows Audi to employ the same headcount as a UK-based team despite the 40% wage premium in Hinwil. This has made Mattia Binotto’s compensation—estimated at $8.5 million—a strategic investment in navigating these complex new financial parameters.

However, Haas team principal Ayao Komatsu noted that “everybody” opposes the Swiss offset, arguing that “everybody chooses where to set up the team”. The debate highlights tensions between regulatory equity and competitive pragmatism—a tension that will define Audi’s entry strategy and their ability to attract top engineering talent to Switzerland.

The 2026 Grid Disruption: Corporate Entries and Risk Management Premiums

The 2026 season represents an inflection point for F1 executive compensation. The convergence of new engine regulations, Audi’s corporate entry, and the expanded $215 million cost cap has elevated team principals from operational managers to specialized risk managers commanding premium compensation. Unlike Fortune 500 CEOs who navigate quarterly earnings cycles, F1 principals manage real-time global engineering R&D with legally binding spending ceilings—a constraint that makes leadership quality the primary differentiator between championship contention and midfield anonymity.

Audi’s entry has particularly disrupted the talent market. Corporate-backed teams historically pay premium salaries to attract proven leadership, and Audi’s Swiss base adds a 35-45% wage premium that compounds this inflation. The cost cap offset mitigates but does not eliminate this structural cost disadvantage, meaning Audi must offer competitive packages to attract talent to Hinwil rather than Oxfordshire or Maranello.

The “equity moat” remains the defining distinction. Wolff’s ownership model—rare in modern F1—aligns his financial interests with long-term franchise value appreciation rather than short-term salary maximization. His $2 billion equity stake generates wealth through capital appreciation and dividends, not base compensation. Employee principals like Vasseur, Stella, and Mekies, however dependent on salary and performance bonuses, face inherent caps on wealth accumulation regardless of team success.

For institutional investors evaluating F1 franchise valuations, the compensation architecture reveals governance quality. Teams with owner-principals demonstrate aligned incentives; teams with highly-paid employee principals may face principal-agent conflicts as executives optimize for personal compensation within cost-constrained environments. The 2026 regulations, by exempting top executive salaries while capping engineering spend, inadvertently amplify this governance distinction—making leadership selection the critical strategic variable in the sport’s new financial era.

Executive Compensation Architecture: F1 vs. Fortune 500

Unlike Fortune 500 CEOs who manage quarterly earnings and stock price performance, F1 Team Principals operate within a uniquely constrained environment: a legally binding $215 million annual budget cap on car development, with zero ability to raise external capital for operational expansion. Their compensation—exempt from the cost cap—reflects risk management under extreme resource constraints, where a single strategic error in wind tunnel allocation or power unit development can eliminate championship contention for an entire regulatory cycle.

Executive Compensation Tier List (2026)

| Rank | Executive / Principal | Team | Base Salary | Est. Total Comp | Net Worth | Equity Stake | Key Differentiator |

|---|---|---|---|---|---|---|---|

| 1 | Adrian Newey | Aston Martin | $40M (€37M) | $40M+ | $250M+ | Vesting Options | Highest off-track salary in F1 history; IP Architect. |

| 2 | Zak Brown | McLaren | $13M (€12M) | $15M+ | $120M+ | 0% | Commercial powerhouse; highest non-principal CEO salary. |

| 3 | Toto Wolff | Mercedes | $8.7M (€8M) | $65M+ | $2.7B | ~28% (Owner) | Owner-operator; $53M dividend yield (2025). |

| 4 | Fred Vasseur | Ferrari | $8.7M (€8M) | $10.5M | $12M | 0% | Prestige premium for managing Hamilton Era Year 2. |

| 5 | Mattia Binotto | Audi (Sauber) | $8.7M (€8M) | $9.5M | $20M | 0% | Navigating the 40% “Swiss Offset” subsidy. |

| 6 | James Vowles | Williams | $8.1M (€7.5M) | $9M | $7M | Retention Equity | Leading the Dorilton Capital long-tail rebuild. |

| 7 | Laurent Mekies | Red Bull Racing | $7.6M (€7M) | $10M | $5M | Leadership Equity | Promoted following Horner’s 2025 “Liquidity Event.” |

| 8 | Andrea Stella | McLaren | $6.5M (€6M) | $8.5M | $4M | 0% | Defending 2024 Constructors’ Champion principal. |

| * | Christian Horner | Ex-Red Bull | N/A | N/A | $150M+ | 0% (Cashed Out) | Received $100M settlement; target: Cadillac 2027. |

*Christian Horner was dismissed from Red Bull Racing in July 2025. Figures reflect final 2025 compensation.

Frequently Asked Questions: 2026 Financial Regulations

Who is the highest-paid F1 team principal in 2026? +

Does Toto Wolff own the Mercedes F1 team? +

Are executive salaries included in the $215M cost cap? +

Related Forensic Wealth Audits

- • Broadcasting Capital: Sky Sports Pundit Salaries & Net Worth Audit

- • The Klutch Effect: Analyzing Rich Paul’s $1.4B Agency Value & Net Worth

- • Legacy Assets: A Comparative Study of British Sports Icons’ Net Worth