Executive Summary

Simon Halabi’s trajectory from $4.3 billion peak net worth (2007) to High Court bankruptcy (April 2010) represents not market misfortune but a systemic failure in Loan-to-Value (LTV) discipline and illiquid asset allocation. This audit deconstructs how the Syrian-born property magnate’s concentration in unrenovatable Grade I-listed heritage assets (Mentmore Towers) and over-leveraged commercial stakes (The Shard, Esporta) created a liquidity trap that annihilated generational wealth in 36 months. Crucially, Halabi’s 2008-2010 collapse serves as a lead indicator for the 2025-2026 Commercial Real Estate (CRE) reset, where high carrying costs on unrenovated heritage assets are forcing UHNW individuals into fire sales to protect liquid cores.

Forensic Asset Profile: Simon Halabi ($4.3B Portfolio Collapse)

Who Owns Mentmore Towers in 2026? The Economic Reality of “White Elephant” Heritage Assets

As of Q1 2026, Mentmore Towers remains the ultimate cautionary tale for the “Heritage Trap.” While title deeds still link the 1854 Rothschild estate to Simon Halabi via Mentmore Towers Ltd, the property’s true “owner” is its own carrying cost. Currently classified as Priority A on the Heritage at Risk Register, the mansion represents a £160M valuation that has effectively hit zero due to unexecutable planning permissions and $0$ revenue generation. In a 2026 environment of high interest rates, this “White Elephant” serves as a lead indicator: when legacy assets are un-renovatable, they cease to be “Shadow Wealth” and become high-velocity capital sinks.

Mentmore Towers Planning Permission: Why the £160M Hotel Conversion Failed

Halabi’s 1999 acquisition of Mentmore Towers—the former Rothschild estate built by Sir Joseph Paxton in 1854—exemplifies the dangers of heritage real estate without viable exit strategies. The Grade I-listed mansion, featuring Jacobethan architecture and interiors by Paxton, carried development potential that proved legally and economically unexecutable.

The Planning Permission Friction:

In 2004, Halabi secured permission to convert Mentmore into a 171-suite luxury hotel with a new wing containing conference facilities and a spa. However, local opposition and High Court injunctions delayed construction until 2007. By the time work commenced, the 2008 financial crisis had frozen credit markets and collapsed luxury hospitality valuations.

The Carrying Cost Trap:

Unlike income-generating commercial assets, Mentmore required continuous capital expenditure with zero revenue offset:

- Structural deterioration: Roof and chimney failures allowing water ingress into the main hall

- Security costs: Regular trespasser incidents requiring Thames Valley Police intervention (most recently May 2024)

- Heritage compliance: Historic England Priority A classification (“immediate risk of further rapid deterioration”) mandating urgent but unfunded repairs

The abandonment of Mentmore Towers serves as a critical lead indicator for the current high-stakes London development cycle. While projects like the Earls Court Masterplan enter their construction phase in 2026 with a projected £10 billion GDV, they face the same systemic risks that liquidated Halabi: regulatory friction, planning permission “lag,” and the volatile carrying costs of prime Zone 1 acreage.

By April 2022, reports described Mentmore as “abandoned” and “left to rot”—a £160 million asset (peak valuation) rendered valueless by regulatory friction and capital constraints.

The Shard Original Investors and the 77% Haircut: A Masterclass in Commercial Over-Leverage

The inclusion of The Shard in the Protractor Portfolio was meant to be Halabi’s crown jewel; instead, it became his most expensive exit. In January 2008, a 33% stake valued at £130M was liquidated for a mere £30M to Qatari sovereign funds—a 77% haircut necessitated by a 10-day ultimatum from consortium banks. This brief deconstructs the domino effect of cross-collateralization, where a breach in the Esporta health club debt covenants triggered a forced fire sale of a “Spotlight Reach” asset. For 2026 investors, the lesson is clear: even a Renzo Piano-designed landmark cannot survive a structural LTV (Loan-to-Value) inversion.

LTV Covenant Breaches: How Cross-Collateralized Debt Liquidated the Protractor Portfolio

Halabi’s property empire relied on cross-collateralized debt structures that amplified single-asset failures into portfolio-wide insolvency. His one-third stake in The Shard—acquired alongside Irvine Sellar and CLS Holdings—illustrates the liquidity crisis dynamics.

The Shard Fire Sale:

In January 2008, Halabi sold his Shard stake for £30 million to Qatari investment funds—down from a £130 million valuation six months prior. This 77% haircut was necessitated by pressure from consortium banks who gave Halabi 10 days to sell or face foreclosure.

The Esporta Catalyst:

The £460 million purchase of Esporta health clubs in 2007—funded partly by Irish Nationwide Building Society—created the critical rupture with Société Générale, his primary institutional creditor. When Esporta entered administration in late 2007, Halabi lost £120 million of personal capital and damaged the credit relationships necessary to refinance his Protractor (White Tower) portfolio.

The Negative Equity Spiral:

By June 2009, Halabi’s Protractor portfolio—comprising nine London commercial properties including Aviva Tower and Leadenhall Court—had fallen 50% in value. The £1.15 billion loan was secured against assets now worth £929 million, triggering covenant breaches and liquidation orders. Halabi’s structural failure was fundamentally a lack of defensive equity floors. Unlike the systemized Frank Lampard Family Office Architecture, which utilizes “wealth buckets” and low-leverage protocols to insulate capital from macro shocks, Halabi’s portfolio was cross-collateralized to the point of brittleness.

Jersey Property Unit Trusts (JPUTs) and Asset Protection: Forensic Lessons from the Ironzar II Litigation

The Ironzar II Trust litigation was once thought to be a private offshore dispute, but the March 20, 2026, amendment to the Trusts (Jersey) Law 1984 has turned it into a mandatory case study for estate managers. The 2022 Privy Council ruling effectively dismantled the “Fortress” model of JPUTs, clarifying that former trustees and secured creditors rank equally in insolvent distributions. While Halabi utilized these structures to obscure his “Shadow Wealth,” modern AI-driven forensic accounting and 2026 legislative shifts have made these opaque shells transparent, requiring a multi-layered cryptographic approach to true asset protection in the digital age.

The Jersey Trust Litigation

Halabi utilized Jersey-based discretionary trusts—specifically the Ironzar II Trust—to obscure ultimate ownership of remaining assets. However, the 2022 Privy Council ruling in Equity Trust (Jersey) Ltd v Halabi established that current and former trustees rank equally in insolvent trust distributions, complicating Halabi’s executor efforts to prioritize claims.

The case centered on £18 million in settlement costs that former trustees sought to recover from the trust fund. Halabi, as executor of the settlor’s estate and new trustee, argued for pari passu distribution, which would have reduced the former trustee recovery from £6 million to £330,000. The Privy Council ruling against Halabi clarified trustee lien priorities in insolvent Jersey trusts.

2026 Legislative Impact:

In March 2026, Jersey amended the Trusts (Jersey) Law 1984—directly responding to the Halabi litigation—to confirm that secured creditors take priority over trustee liens. This legislative clarification protects lenders to Jersey Property Unit Trusts (JPUTs) but limits the asset protection strategies Halabi attempted to deploy.

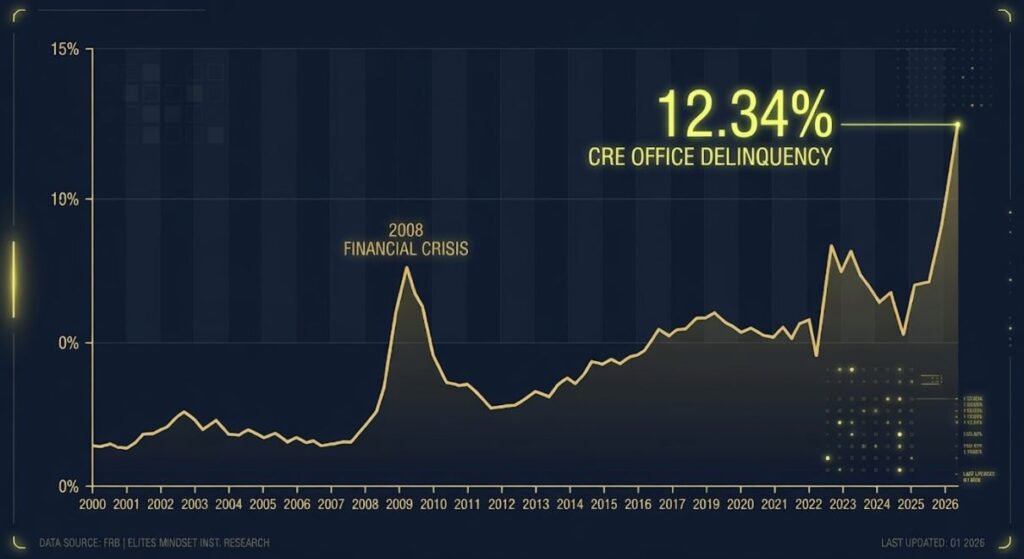

The 2026 Commercial Real Estate (CRE) Delinquency Spike: Why Halabi’s Failure is History Repeating

History is currently rhyming with a 12.34% delinquency rate. In January 2026, the office sector reached its highest distress level since the 2008 crash, mirroring the exact “liquidity trap” that annihilated Halabi’s $4.3B empire. The “2026 High-Interest Lag” is creating a binary market: liquid cores are being defended at all costs, while un-renovated, low-yield commercial assets are being abandoned to creditors. By auditing the Halabi collapse, we reveal the blueprint for the current reset, proving that negative equity spirals are not a product of bad luck, but of failing to maintain a defensive equity floor in a rising-rate environment.

The CRE Reset Parallel

Halabi’s 2008-2010 collapse prefigures the 2025-2026 Commercial Real Estate reset. While 2026 capital markets show stabilization with improving debt availability, the office sector remains distressed with delinquency rates hitting 12.34% in January 2026—the highest since tracking began in 2000.

The Heritage Asset Liquidity Trap:

Unlike the rigorous Capital Sequestration models seen in Bel Air 90077 audits, Halabi’s portfolio lacked defensive equity floors to weather macro-economic shocks. Mentmore Towers acted as a capital sink with high operational burn rates that could not be liquidated quickly to satisfy margin calls on commercial properties—a liquidity trap now repeating in 2026 as UHNW individuals face “fire sales” of heritage assets to protect liquid cores.