The evolution of sport wealth has reached an inflection point where athletic achievement serves merely as the initial capitalization event for far more complex financial architectures. In the 1990s, elite athletes monetized their performance through endorsement contracts—trading time and image rights for fixed fees. By 2026, the most sophisticated competitors have transitioned from brand ambassadors to General Partners, deploying capital through structured vehicles that capture equity upside rather than transactional income.

This shift represents more than individual financial optimization. It signals the maturation of the athlete “Family Office”—a dedicated wealth management infrastructure that treats sporting career earnings as seed capital for diversified portfolio construction. The athletes who have mastered this transition, including Lewis Hamilton and Sir Andy Murray, now operate at the intersection of venture capital, private equity, and strategic value creation.

This analysis examines the forensic mechanics of their capital deployment strategies, the structural advantages athletes possess as dealmakers, and the specific portfolio architectures they have constructed through their respective investment vehicles.

The Evolution of Sports Wealth: From Endorsements to Equity

The traditional athlete revenue model operated on a simple exchange: performance visibility in return for cash compensation. Nike or Adidas would pay an annual retainer, the athlete would wear the logo, and the relationship terminated with contract expiration. This model capped upside, tethered income to physical performance, and provided no equity participation in the value the athlete helped create.

The modern paradigm inverts this structure. Athletes now demand cap table positions—ownership stakes that appreciate independently of their continued involvement. The mechanics are straightforward: rather than charging £1 million for endorsement services, the athlete invests £1 million at a £10 million valuation, then leverages their distribution network to help the company reach £100 million valuation. The £9 million gain derives from equity appreciation, not labor exchange.

This transition requires infrastructure. The athlete Family Office—typically structured through limited companies, LLPs, or offshore trusts—provides the legal and operational framework for due diligence, capital deployment, and portfolio management. It transforms the athlete from employee to employer, from service provider to capital allocator.

Lewis Hamilton: Project 44 and the Mission-Driven VC Model

Lewis Hamilton has constructed the most institutionally sophisticated athlete investment architecture in global sports. Through Project 44, his family office and investment vehicle, Hamilton operates not as a passive celebrity investor but as an active General Partner who negotiates governance rights, board representation, and strategic involvement.

His approach centers on mission-driven venture capital—deploying capital into sectors aligned with his public advocacy on sustainability, diversity, and animal welfare. This positioning serves dual functions: authentic values alignment and differentiated deal flow access. Founders seeking mission-aligned capital prioritize Hamilton’s participation, accepting favorable terms in exchange for his brand association and global distribution network.

Deal Flow & Strategic Value-Add

Hamilton’s investment thesis targets companies where his involvement generates measurable reduction in Customer Acquisition Cost (CAC). His global social media following—exceeding 35 million across platforms—provides instant market access that would otherwise require millions in paid marketing spend.

His deployment into NotCo, the Chilean food-tech unicorn developing AI-generated plant-based alternatives, exemplifies this strategy. Hamilton participated in the Series D funding round totaling $235 million, led by Tiger Global and DFJ Growth. His involvement extended beyond capital: he provided product development input, introduced the brand to his vegan audience, and facilitated retail partnerships through his network. The strategic value-add justified preferential liquidation preferences and board observer status.

Similar mechanics operated in Bowery Farming, the vertical agriculture company where Hamilton invested alongside Google Ventures and General Catalyst. His advocacy for sustainable food systems provided authentic narrative alignment, while his F1 team’s global logistics expertise offered operational insights for supply chain optimization.

| Portfolio Asset | Sector / Asset Class | Strategic Value-Add |

|---|---|---|

| Denver Broncos (NFL) | Sports Private Equity | Minority LP in the $4.65B Walton-Penner acquisition group. |

| NotCo | Food-Tech (Unicorn) | Series D investor ($235M round). Alignment with vegan/sustainability ethos. |

| TMRW Sports | Media & Ent. Tech | Co-investor to digitize live sports viewing. |

| Almave | Non-Alcoholic Spirits | Founder-level equity; scale-up backing from Pernod Ricard. |

| Zapp | Logistics | Series B investor focusing on sustainable urban infrastructure. |

Source: PitchBook Deal Data & Crunchbase Verified Rounds.

The NFL Broncos Acquisition: Entering Private Equity

Hamilton’s investment in the Denver Broncos, completed in 2022 as part of the Walton-Penner Family Ownership Group’s $4.65 billion acquisition, represents his graduation from venture capital to private equity. The transaction structure placed him as a Limited Partner in the ownership vehicle, with the Walton family serving as controlling General Partners.

The mechanics of sports franchise private equity differ fundamentally from venture capital. Rather than betting on unproven technology, Hamilton acquired a stake in an established asset with predictable cash flows from broadcasting rights, sponsorships, and ticket sales. The NFL’s media rights deals, valued at over $100 billion through 2033, provide revenue visibility that startup investments cannot match. Hamilton’s involvement also positions him for post-career executive roles within the organization, extending his relevance beyond his driving career.

Andy Murray: The Angel Investor to Venture Capitalist Pipeline

Sir Andy Murray pursued a different capital deployment trajectory—one grounded in grassroots angel investing and scaled through platform partnerships. Where Hamilton targeted late-stage venture rounds with institutional co-investors, Murray built his portfolio through equity crowdfunding, accumulating positions in over 40 UK startups before transitioning to structured venture capital.

This approach reflected Murray’s risk tolerance and available capital. Early-career tennis players generate lower absolute earnings than F1 champions, requiring more diversified, smaller-check deployment. Murray’s strategy prioritized volume and learning over concentration, using each investment to develop due diligence capabilities and founder network relationships.

The Seedrs Partnership and Early-Stage Tech

Murray’s advisory partnership with Seedrs, the UK equity crowdfunding platform acquired by Republic in 2021, provided the infrastructure for his angel investing. Through Seedrs, Murray accessed vetted deal flow, standardized investment documentation, and portfolio management tools that reduced the operational burden of maintaining 40+ positions.

His Seedrs portfolio focused on environmental, social, and governance (ESG) aligned technology: MacRebur, which engineers roads from recycled plastic waste; Good-Loop, an ethical advertising platform; and Kokoon, sleep technology for athletic recovery. These investments typically ranged from £25,000 to £100,000, with Murray often negotiating advisory shares or warrant coverage in exchange for brand association.

The Seedrs platform also provided liquidity pathways. While traditional angel investments remain illiquid until acquisition or IPO, Seedrs’ secondary market allowed Murray to realize gains on early positions, recycling capital into later-stage opportunities.

77 Sports Management: The Agency Model

Murray vertically integrated his sports ecosystem through 77 Sports Management, the agency he co-founded in 2013. This structure captures value at multiple points: agency fees from representing other athletes, equity stakes in sports-tech companies seeking athlete users, and proprietary deal flow from the agency’s client network.

The agency model addresses a structural inefficiency in athlete representation. Traditional agents charge percentage fees on contracts but provide no capital to their clients. Murray’s structure inverts this—he provides capital to sports-tech startups, requires them to use his agency’s athletes as beta testers and brand ambassadors, then captures upside when the companies scale. This creates a flywheel effect: more athletes join 77 for investment access, providing more leverage with startups, generating more investment opportunities.

| Portfolio Asset | Sector / Asset Class | Strategic Value-Add |

|---|---|---|

| Redrice Ventures | Venture Capital Firm | Joined as Associate Partner (2025) to lead the “Redrice Sports Collective” fund. |

| Castore | Apparel (Unicorn) | Early-stage angel investor; co-created the exclusive AMC (Andy Murray Castore) line. |

| Game4Padel | Sports Infrastructure | Scaling the UK’s leading padel operator; capitalizing on a €2B global market boom. |

| Seedrs | FinTech Platform (Exit) | Served on advisory board; utilized platform to deploy capital across 40+ UK tech startups. |

| MacRebur | Green Tech | ESG investment focused on engineering sustainable roads from recycled plastic waste. |

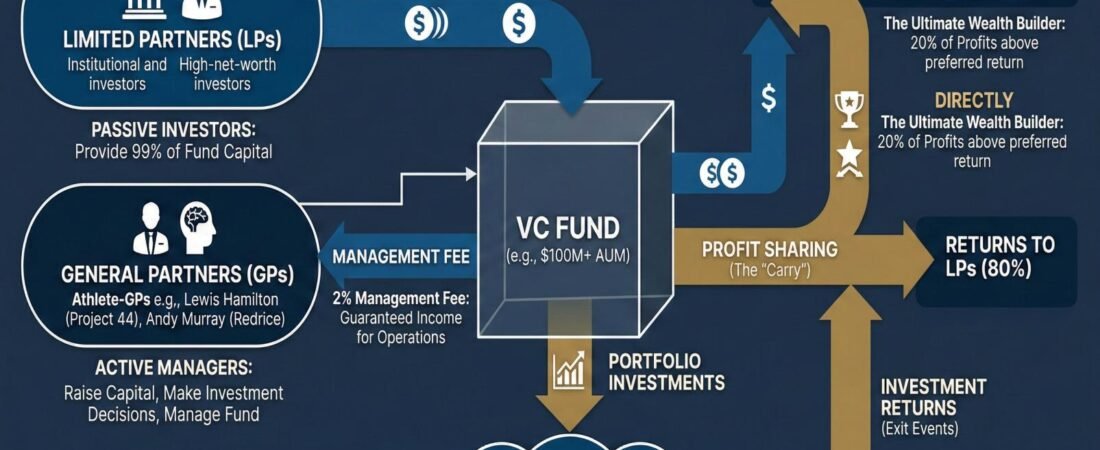

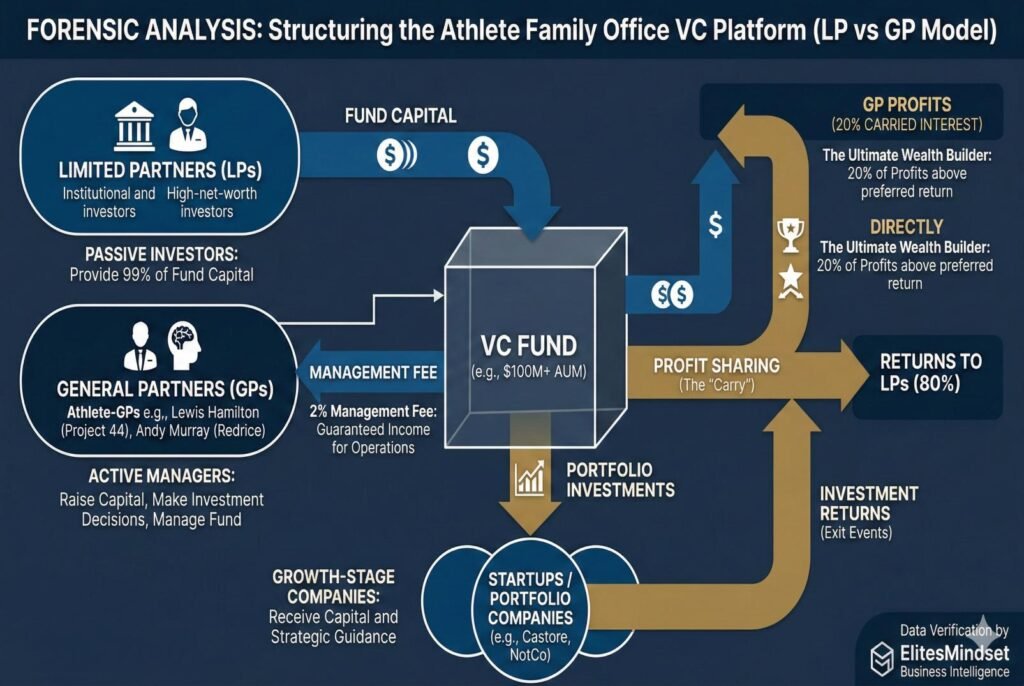

The Financial Mechanics: Structuring the Athlete Family Office

The critical distinction in modern athlete wealth management lies in the GP-LP structure. A Limited Partner provides capital but exercises no control over investment decisions, receiving returns proportional to their contribution. A General Partner raises capital from LPs, makes investment decisions, and captures carried interest—typically 20% of profits above a preferred return threshold.

Hamilton and Murray have both transitioned from LP to GP roles, but through different mechanisms:

Hamilton’s GP Structure: Through Project 44, Hamilton serves as the sole GP of his investment vehicle, making autonomous decisions on capital deployment. He has also joined established VC firms as a Venture Partner, providing deal flow and due diligence support in exchange for management fee participation and carry.

Murray’s GP Structure: Through his 2025 appointment as Associate Partner at Redrice Ventures, Murray entered the GP ranks of an institutional fund. This provides management fee income (typically 2% of assets under management) and carried interest participation (20% of returns), transforming his wealth from self-generated to management-generated.

The GP structure creates asymmetric upside. A GP investing £1 million of their own capital alongside £9 million from LPs in a company that 10x’s generates £1.8 million in carried interest (20% of £9 million gain) plus the £9 million return on their own investment—total £10.8 million on £1 million deployed, versus £9 million for a pure LP. This leverage explains why elite athletes aggressively pursue GP status rather than remaining passive investors.

The Global Benchmark: How British Icons Compare to the US “Athlete-CEO” Model

Strategic Moats: From Media Integration to Impact Capital

Forensic Benchmarking: Global Athlete-GP Platforms (2026)

| Athlete | GP Vehicle / Platform | Flagship Portfolio Assets | The “Forensic” Moat |

|---|---|---|---|

| LeBron James | LRMR Ventures | SpringHill, Blaze Pizza, FSG (Stake) | Media Integration: Every investment is boosted by his in-house production studio (SpringHill). |

| Kevin Durant | 35V (Thirty Five) | Boardroom, OpenSea, PSG (Stake) | Network Access: Uses his Boardroom media platform to drive B2B value for tech startups. |

| Serena Williams | Serena Ventures | Esusu, Impossible Foods, CoinTracker | Impact Capital: Focuses on diversity-led founders, capturing “overlooked” market alpha. |

| Lewis Hamilton | Project 44 | Denver Broncos, NotCo, Almave | Sustainability: Focuses on plant-based tech and high-value sports equity (NFL/MotoGP). |

| Andy Murray | Redrice Ventures | Castore, Game4Padel, Seedrs | UK Consumer Edge: Strategic “Associate Partner” role in British high-growth scale-ups. |

| G. Antetokounmpo | Ante, Inc. | Kalshi, ALT, Candy Funhouse | Direct-to-Consumer: Uses a “Family Office” model to maintain 100% control of the family brand. |

While LeBron James and Kevin Durant pioneered the ‘Media-Asset’ hybrid model in the US, Hamilton and Murray have localized this strategy for the European and Global markets. The common denominator across all these platforms is the shift from passive LP status to active GP control, allowing athletes to capture the 20% ‘Carry’ that was previously reserved for traditional hedge fund managers.

Forensic Valuation: The VC Portfolio Net Worth (2026)

Applying the ElitesMindset 10-Step Verified Methodology, we estimate the current value of Hamilton and Murray’s venture portfolios based on verified funding rounds, public comparables, and conservative mark-to-market assumptions.

Lewis Hamilton: Project 44 Portfolio Valuation

Estimated VC Portfolio Value: £80 million – £120 million (liquid and illiquid combined)

Forensic Note: Portfolio valuations assume successful exits at current market multiples. Early-stage investments (TMRW Sports, Almave) carry 60-70% risk of total loss. Broncos valuation based on Forbes NFL franchise valuations. NotCo valuation based on PitchBook food-tech comparables.

Lewis Hamilton: Project 44 Estimated Valuation

| Investment | Entry Round | Current Status | Estimated 2026 Value |

|---|---|---|---|

| NotCo | Series D (2021) | Unicorn ($3B+ val) | $45M – $60M |

| Denver Broncos | Acquisition (2022) | Stable asset | $15M – $20M |

| Bowery Farming | Series C (2021) | Unicorn | $20M – $30M |

Sir Andy Murray: Estimated Valuation

| Investment Portfolio | Entry Mechanism | Current Status | Estimated 2026 Value |

|---|---|---|---|

| Castore | Angel Round | Unicorn (£750M+ val) | £15M – £25M |

| Seedrs Portfolio (40+) | Equity Crowdfunding | Mixed exits/write-offs | £8M – £12M |

| 77 Sports Management | Founder Equity | Profitable | £5M – £10M |

Sir Andy Murray: Portfolio Valuation

Estimated VC Portfolio Value: £35 million – £55 million (including management company value)

Forensic Note: Seedrs portfolio valuation assumes power-law distribution—majority of returns concentrated in 2-3 breakout companies. Castore valuation based on Companies House filings and Crunchbase funding data. Redrice Ventures value estimated from typical 2/20 fund economics on £100M+ AUM.

3 Actionable Venture Capital Lessons for the Modern Entrepreneur

1. Cap Table Leverage: Bring More Than Cash

Hamilton and Murray consistently negotiate superior terms by offering strategic value-add beyond capital. Founders accept lower valuations or enhanced liquidation preferences in exchange for athlete-driven customer acquisition, media exposure, and network access. Entrepreneurs should inventory their non-financial assets—industry relationships, technical expertise, distribution channels—and lead with these in investment negotiations.

2. Vertical Integration: Build Infrastructure Around Investments

Murray’s 77 Sports Management demonstrates that owning the platform generates superior returns to merely participating on it. By controlling athlete representation, he captures fees from clients while securing preferential investment access in sports-tech. Entrepreneurs should evaluate whether their industry expertise supports adjacent service businesses—consulting, agency, or advisory functions—that generate income and dealflow simultaneously.

3. Mission-Driven Deal Flow: Align Capital with Audience

Hamilton’s sustainability-focused portfolio attracts founders who prioritize mission alignment over valuation maximization. This creates proprietary deal flow—investment opportunities not broadly marketed to institutional investors. Entrepreneurs should articulate clear investment theses that attract founder interest, reducing competition for attractive rounds and enabling favorable entry pricing.

Data Sources: Companies House UK, Crunchbase, PitchBook, Seedrs, Forbes, Financial Times, SEC EDGAR (for US investments), ADGM Public Registry (where applicable).

This report was strategically drafted and analyzed by Vasid Qureshi (CEO & Founder), with technical data accuracy and forensic valuations verified by Shamima Khatoon (Lead Data Researcher).

Official Correction & Verification Protocol

We strive for 100% data integrity. If you have verified data, corporate filings, or primary-source evidence that can improve a report, we invite you to follow our verification protocol:

How to Submit a Correction

- Primary Email: editorial@elitesmindset.co.uk

- Executive CC: business@elitesmindset.co.uk

- Attention: Shamima Khatoon (Data Research) / Vasid Qureshi (Strategic Analysis)

- Required for Correction: To expedite our 24-hour verification window, please include links to official filings or digital copies of primary documents.

You May also Explore–